You may feel your Texas family law case was handled unfairly. After a long and difficult trial, the judge's final order regarding your home and mortgage can feel like an impossible burden. If the court has ordered you to assume or refinance a mortgage you cannot afford, or structured the property division in a way that is financially unworkable, you are not out of options. The Texas appeals process exists to correct these kinds of mistakes.

This guide explains how assuming a mortgage works in a Texas divorce and, more importantly, how an appellate attorney can help challenge a court order that is unjust or ignores financial realities. While the trial court has broad discretion, its decisions must be based on the evidence and the law. When they are not, you have the right to seek a fair outcome through an appeal.

What You Can Appeal in a Texas Divorce Property Division

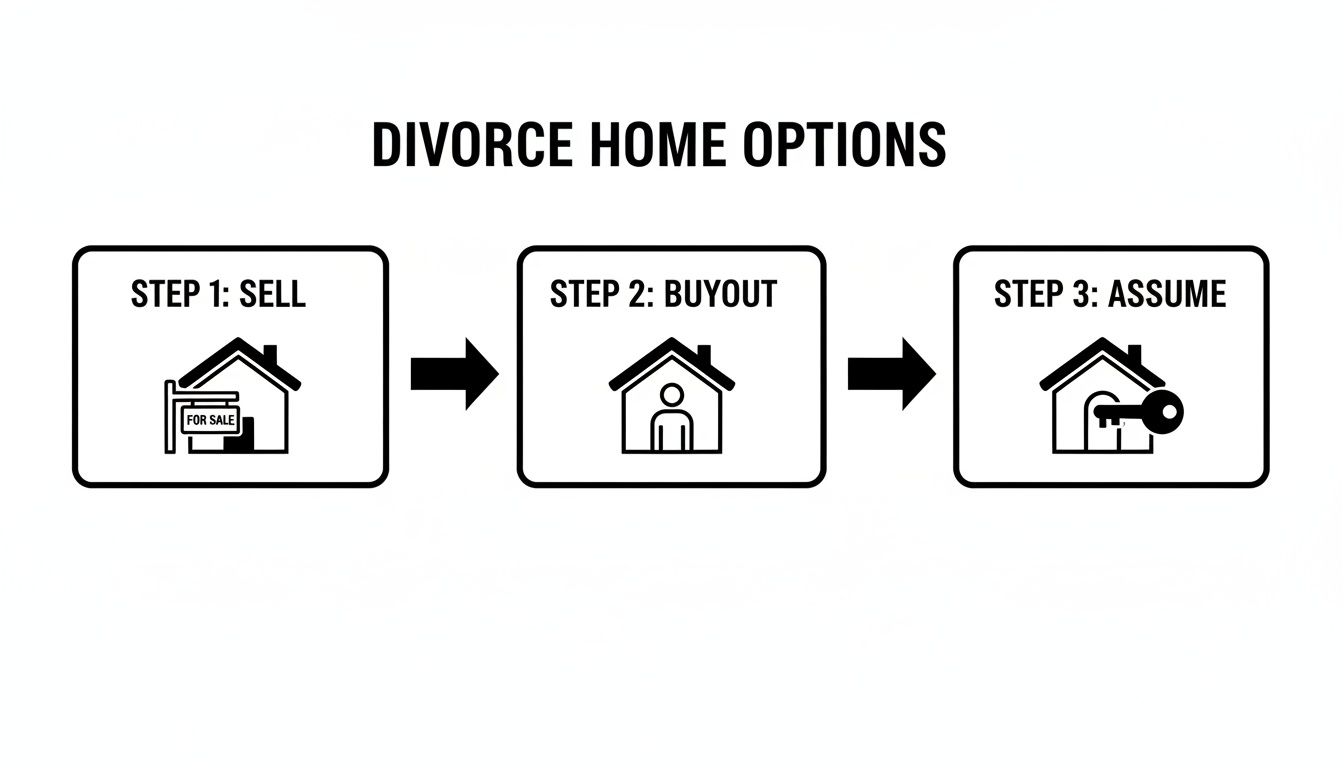

When a marriage ends, you're usually faced with three main paths for the house: sell it and split the proceeds, have one spouse buy out the other's share, or have one spouse formally assume the mortgage. In Texas, the house is typically considered community property, which means it must be divided in a "just and right" manner.

You can find a deep dive into how Texas community property works on our site, but the key takeaway is that the division must be equitable. A critical point that many people misunderstand is that a divorce decree ordering one spouse to pay the mortgage does not automatically remove the other spouse's name from the loan. The original contract with the lender remains in effect, meaning both parties are legally responsible until the bank formally grants a release of liability.

If the trial court's order creates an inequitable result—for example, by ordering a property division that is impossible to execute—it may be considered a reversible error.

Your Options for the Family Home

The best route for you is going to come down to your finances, the specifics of your mortgage, and what the final divorce decree says. This chart lays out the three main choices you'll be weighing.

Each of these paths has its own unique financial and legal consequences, so it's important to understand what you're getting into before making a final call.

Common Reversible Errors in Property Division

A divorce decree is not set in stone if it contains a significant legal mistake. Texas family law appeals often center on correcting unfair property divisions. If a trial judge ordered a division of your home that ignores the evidence, misapplies the law, or puts an unconscionable burden on you, that decision can be challenged. This is the core of appellate advocacy: ensuring the law was applied fairly and correctly based on the trial record.

Common examples of reversible errors in property division cases include:

- Ordering a spouse to assume or refinance a mortgage without evidence they can financially qualify.

- Mischaracterizing separate property as community property, leading to an improper division.

- Making significant mathematical errors in calculating the value of the home's equity.

- Failing to divide the community estate in a "just and right" manner, which is known as an abuse of discretion.

Understanding the Standard of Review in a Mortgage Assumption Case

If your divorce decree orders you to keep the house, you must also handle the mortgage. Simply taking over the payments is not enough. You must go through a formal process called mortgage assumption to remove your ex-spouse's name from the loan and release them from all legal and financial responsibility. This is a critical step to truly separate your financial lives.

The first question is whether your loan is even assumable. Government-backed loans like FHA, VA, and USDA loans often are. Most conventional loans, however, contain a "due-on-sale clause," which allows the lender to demand full payment if the property is transferred.

A federal law, the Garn-St. Germain Depository Institutions Act of 1982, provides a crucial exception. It prevents lenders from enforcing a due-on-sale clause when a property is transferred to a spouse as part of a divorce settlement. This law is a key tool in assuming a conventional mortgage.

You Still Have to Qualify on Your Own

Just because the law allows an assumption does not mean the bank will automatically approve it. The lender will put your finances under a microscope to ensure you can carry the loan on your own. This involves verifying your income, checking your credit, and calculating your debt-to-income (DTI) ratio.

This is where many unfair trial court orders originate. A judge may order one spouse to assume a loan without properly considering the evidence of whether they can actually qualify. If the evidence presented at trial clearly showed you could not qualify, but the judge ordered it anyway, this could be an "abuse of discretion."

What is "Abuse of Discretion"?

In plain English, "abuse of discretion" is a legal term for when a trial judge makes a decision that is arbitrary, unreasonable, or made without reference to guiding rules and principles. Forcing a spouse to take on a mortgage that the evidence proves they cannot afford is a classic example. An appellate court reviews the trial record to determine if the judge's decision was so unfair that it requires correction.

Preparing for the Appellate Process

If you believe the court abused its discretion, the appeal process begins with a careful review of the trial record—the official account of what happened in court. An appellate attorney will examine every document and piece of testimony to build a case. The necessary documents include:

- Your Final Divorce Decree: This document must clearly state that you were awarded the property and are responsible for the mortgage.

- The Lender's Assumption Application & Denial: If you were denied, this paperwork is crucial evidence.

- Financial Records: Pay stubs, bank statements, and tax returns submitted at trial are vital to showing your financial reality.

- The Reporter's Record: This is the word-for-word transcript of the trial testimony.

This evidence is compiled to create a formal legal argument, called a brief, which explains to the appellate court precisely how the trial judge made a reversible error.

Mortgage Assumption Versus Refinancing: The Financial Stakes

When you are awarded the home in a divorce, you face a critical decision: assume the existing mortgage or refinance it into a new loan. Both options can remove your ex-spouse's name from the debt, but they have vastly different financial implications.

Assuming the mortgage allows you to keep the original loan's interest rate and terms. In a high-interest-rate environment, this can be a significant financial advantage. Refinancing, on the other hand, involves taking out a brand-new loan to pay off the old one. This is often necessary to buy out your ex-spouse's share of the home's equity, but it means you will be subject to current interest rates and new closing costs.

Why This Could Be a Reversible Error

The financial stakes here are incredibly high. A home that was affordable on two incomes can become a burden on one, especially if refinancing forces you into a much higher interest rate.

Consider this example: if your current mortgage has a $300,000 balance at a 2.5% interest rate, refinancing at a new rate of 7% would increase your monthly payment from approximately $1,265 to $1,951. This is a 54% increase that could make the home unaffordable. If a Texas court orders you to refinance without properly considering evidence of your ability to afford the new, higher payment, it could be considered a reversible error that can be challenged on appeal.

What is a "Reversible Error"?

In plain English, a reversible error is a legal mistake made by the trial court that was so significant it likely led to an improper outcome. In a property division case, ordering an impossible refinance that is not supported by the financial evidence presented at trial could be such an error. Proving this is a core goal in a Texas divorce appeal.

Comparing Mortgage Assumption vs Refinancing

To make the best choice for your situation, it helps to see the two options laid out side-by-side. This table breaks down the key factors you'll need to consider.

| Feature | Mortgage Assumption | Refinancing |

|---|---|---|

| Interest Rate | Keeps the original, often lower, interest rate. | Secures a new loan at current market rates, which may be higher. |

| Closing Costs | Typically lower, with fewer fees involved. | Requires paying new closing costs, title, and appraisal fees. |

| Equity Buyout | Does not provide cash-out; a separate loan is needed for a buyout. | Can be structured to include cash-out to pay your ex-spouse's equity. |

| Qualification | You must qualify based on your sole income and credit. | You must qualify for a new loan based on current lender standards. |

The best path forward depends on your unique financial picture, the terms of your current loan, and what your divorce decree requires. Before you commit, it’s wise to explore various refinancing options to understand the full landscape of what's available. This will ensure you're making a truly informed decision, not just the easiest one.

What to Do If You Cannot Assume or Refinance

If you have followed the court's order and applied to assume or refinance the mortgage, only to be denied by the lender, you may feel trapped. This is a common and stressful situation, but it is not the end of the story. A denial for financing does not automatically mean you must sell the family home.

An unworkable court order can be challenged. If the trial court created a situation that is impossible to execute, it may have abused its discretion. This is precisely the type of issue that the appellate process is designed to correct.

Challenging Unworkable Court Orders

When a trial court issues an order that is not practical in the real world—such as forcing one spouse to take on a mortgage they cannot possibly qualify for—it may have committed a reversible error. An improperly structured property division can lead to ruined credit, foreclosure, and even bankruptcy. If you're in a position where you can't assume or refinance, it's a good time to start understanding the differences between Chapter 7 and Chapter 13 bankruptcy and what that could mean for your home.

Here are other legal tools that may be considered, though some come with significant risks:

- Structured Buyout: Negotiating to buy out your ex-spouse's equity over time with a legally enforceable payment plan.

- Owelty Lien: A lien is placed on the property to secure the equity owed to your ex-spouse. This allows you to finance only the amount of the lien, which may be easier to qualify for than a full refinance.

- Indemnity Agreement: An agreement to make all mortgage payments and protect your ex-spouse from financial harm if you default.

An indemnity agreement is a promise, not a shield. It does not remove your ex-spouse's name from the loan. If you miss a payment, the lender will report it on both of your credit reports, damaging your ex-spouse's credit regardless of your agreement. A court order relying on such a risky arrangement may be considered unjust.

If you believe the judge’s order was unjust and ignored the financial evidence you presented, it is time to consult with an appellate attorney. They can review the trial record to determine if the judge’s decision created an unfair and unworkable situation that could be successfully challenged on appeal.

How a Texas Appellate Attorney Can Help

A trial court judge's ruling on your home and mortgage is not necessarily the final word. If your divorce decree forces you into an impossible financial corner, you have the right to seek justice. An unfair outcome is not something you have to accept, especially when it jeopardizes your financial stability.

Perhaps the decree orders you to assume a mortgage you clearly cannot afford, or the judge made a critical error in calculating the home's equity. These are not minor details; they are potentially serious legal mistakes that may constitute a reversible error.

Finding Reversible Error in the Trial Record

An appeal is not a new trial. We do not present new evidence or call new witnesses. Instead, an appellate attorney's job is to conduct a meticulous review of the trial record—every piece of testimony, every exhibit, and every ruling—to pinpoint a reversible error. This is a legal mistake so significant that it likely led to an unjust outcome.

Our entire focus is on the law and how the trial judge applied it to the facts presented in your original case. In property division appeals, these errors often include:

- Mischaracterizing Property: Incorrectly classifying separate property (like an inheritance) as community property and dividing it improperly.

- Ignoring Key Evidence: Disregarding clear evidence that a spouse could not qualify to refinance or assume a mortgage.

- Valuation & Math Errors: Making costly mistakes in calculating the value of an asset, which skews the entire division.

What is an "Abuse of Discretion"?

In Texas, many property division appeals hinge on the legal standard of "abuse of discretion." This means the judge's decision was so arbitrary, unreasonable, or disconnected from the facts and law that it was fundamentally unfair. Forcing you to take on a mortgage that the evidence showed was financially impossible for you to handle could be a classic example of this.

An appellate court will not simply substitute its judgment for the trial judge's. To win an appeal, we must prove the decision was not just incorrect, but that it fell completely outside the zone of reasonable disagreement and created a truly unjust result.

Our task is to build a persuasive legal argument, presented in a formal document called an appellate brief, to convince the higher court that a significant error occurred. The goal is to have the unfair portion of your decree reversed and sent back to the trial court with instructions to issue a fair and workable order.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.

Common Questions About Mortgage Assumption in a Texas Divorce

Navigating a mortgage after a divorce can feel overwhelming. Understanding your legal responsibilities versus the bank's requirements is the first step toward restoring your financial stability. Here are answers to common questions we encounter in Texas divorce appeals.

Does My Divorce Decree Automatically Remove My Ex-Spouse From the Mortgage?

No. This is the single most critical and dangerous misunderstanding in post-divorce property matters. Your divorce decree is a court order between you and your ex-spouse. Your mortgage is a contract between both of you and the lender. A family court judge does not have the authority to alter that contract.

Until the mortgage is formally assumed by you or refinanced, both of you remain 100% liable for the debt. If payments are missed, the lender can pursue collections against both parties, regardless of what your decree says. The only way to sever that financial tie is with a formal release of liability issued directly by the lender.

What if My Lender Denies My Assumption Application?

A denial from the bank is a setback, but it is not the end of the story. First, request the reason for the denial in writing. It typically relates to income, credit, or debt-to-income ratios. Once you know the reason, you can strategize.

More importantly, from an appellate standpoint, a denial can become key evidence. If your divorce decree required you to assume a loan that the bank has now confirmed is impossible for you to obtain, this strengthens the argument that the trial court's order was an abuse of discretion. An order that knowingly sets a party up for financial failure may be grounds for an appeal.

How Long Does the Mortgage Assumption Process Take?

The mortgage assumption process is not quick. You should be prepared for it to take anywhere from 45 to 90 days, and sometimes longer. The lender treats it like a new loan application, requiring extensive documentation, credit checks, and income verification. Any missing paperwork can cause delays.

Because of this timeline, it is crucial to begin the application process immediately after your divorce is finalized. Do not wait. The sooner you get the paperwork started, the sooner you can get a definitive answer and take the next necessary steps, whether that is completing the assumption or preparing for an appeal.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.