You may feel your case was handled unfairly, especially when a court’s decision on a major asset like a 401(k) threatens your financial future. When you’re facing a divorce in Texas, untangling finances is one of the toughest parts. If a 401(k) is part of the picture, it's often one of the most significant assets you'll need to divide. A critical legal error in this process can have lasting consequences, but the Texas appeals process exists to correct such mistakes and restore fairness.

Under Texas law, any contributions made to that account during the marriage are considered community property and must be divided in a "just and right" manner. This doesn't automatically mean a 50/50 split, but that is the starting point. The entire process hinges on a special legal document called a Qualified Domestic Relations Order (QDRO). If this document is flawed or the court misinterprets the law, you may have strong grounds for an appeal.

What You Can Appeal in a 401(k) Division

It’s completely normal to feel like the financial deck was stacked against you in your divorce. When a major asset like a 401(k) is divided, the court's final decision can ripple through your life for years to come. This is a common worry, and navigating it successfully means understanding Texas appellate procedure and what you can do about an unjust outcome.

In Texas, all retirement funds built up while you were married are presumed to belong to both of you as part of the marital estate. They must be divided fairly—a decision left to the judge's discretion. For many couples, how this asset is split can be the single most important financial outcome of the divorce. If you believe that discretion was abused, an appeal may be your path to justice.

A core concept in community property states like Texas is that both spouses generally have an equal claim to retirement contributions and earnings that accumulated during the marriage. An appeal is not a retrial but a focused review to determine if the trial court correctly applied this and other legal principles to the facts of your case.

Understanding Reversible Error in Property Division

Splitting a 401(k) isn't just about moving numbers on a balance sheet; it's about protecting your financial security. A single mistake or an unfair ruling from the trial court can put the stability you've spent your entire career building at risk. A reversible error is a legal mistake so significant that it likely caused the trial court to reach the wrong conclusion.

This division is a critical piece of the property puzzle, and it’s deeply connected to other financial outcomes. If you're looking at the bigger picture, it helps to understand the potential cost of a divorce in Texas to see how everything fits together.

The legal tool that effectuates the division is the Qualified Domestic Relations Order (QDRO). This is a specific court order sent to the 401(k) plan administrator, telling them how to divide the account. Without a perfectly drafted QDRO that reflects the court’s decree, the division can be executed improperly, leading to massive tax penalties or an incorrect distribution.

If you feel the court got it wrong—maybe it misclassified your separate property as community property or used the wrong valuation dates—you don't have to just accept it. The appellate process exists specifically to correct these kinds of reversible errors and give you a path to a just outcome.

Sorting Community from Separate Property in Your 401k

It’s a gut-wrenching feeling when you look at a court’s final order and realize your finances have been divided unfairly. This often happens when hard-earned retirement savings are misidentified and split incorrectly. In a Texas divorce, one of the biggest financial battlegrounds is often the 401(k), and the real challenge lies in figuring out which part is community property and which is separate.

Getting this right isn’t just about paperwork; it's about making sure the final division is truly "just and right" under the law.

The starting point in Texas is a legal presumption: pretty much everything you and your spouse acquired during the marriage is considered community property. This means any money put into a 401(k) during the marriage—plus all the interest, dividends, and growth on those contributions—belongs to both of you. But this is just a presumption, and it can be challenged with solid evidence.

Defining Your Separate Property

Your separate property is yours alone. The court can't touch it. Texas law is crystal clear about what qualifies:

- What you owned before the wedding: The exact balance in your 401(k) on the day you said "I do" is your separate property.

- Gifts you received: If your parents gave you money and you kept it in a separate account, that's yours.

- Inheritances: Any money or assets you inherited during the marriage belong solely to you.

The problem, especially with a 401(k) that’s been active for years, is that separate and community money gets jumbled together. The law puts the burden of proof squarely on the person claiming something is separate property. You have to prove it, or the court will assume it’s community.

A shockingly common and reversible error happens when a trial court fails to correctly identify and set aside a spouse's separate property. If you can prove the court mistakenly labeled your pre-marital 401(k) funds as community assets, that mistake can be a powerful basis for a successful appeal.

The Critical Process of Tracing

To protect the portion of your 401(k) that is rightfully yours, you have to engage in a process called tracing. This is where you methodically track your separate funds from where they started to where they are now, using financial records as your proof.

It takes meticulous documentation. You need to show that the $50,000 in your account on your wedding day has grown over the years and is still distinct from the contributions made during the marriage.

Let's walk through a real-world scenario.

Imagine you had $75,000 in your 401(k) when you got married 15 years ago. Over those 15 years, you and your employer added another $200,000. Thanks to market gains, the account is now worth $500,000. To protect your separate interest, you’d need to pull out the account statements from around your wedding date to prove that initial $75,000 balance. You might even need a financial expert to calculate how much that original investment grew on its own, completely separate from the marital contributions.

That entire traced amount—the original $75,000 plus all of its growth—is your separate property and is not on the table for division. If you fail to trace it properly, you risk the court treating the whole $500,000 as community property, which would be a devastating financial loss. This is why having complete, organized financial records is your best line of defense.

To better illustrate how these assets are viewed, here’s a breakdown of how the funds in a typical 401(k) are classified.

Community vs Separate Property in a 401k

| Asset Component | Legal Classification in Texas | How It's Treated in Divorce |

|---|---|---|

| Pre-Marital Balance | Separate Property | Belongs solely to the employee spouse and is not divided. |

| Contributions During Marriage | Community Property | Subject to a "just and right" division between both spouses. |

| Employer Matches During Marriage | Community Property | Considered earnings during the marriage; subject to division. |

| Growth on Pre-Marital Balance | Separate Property | The appreciation of separate property remains separate property. |

| Growth on Marital Contributions | Community Property | All earnings on community funds are also community property. |

Understanding this table is key. The growth on your pre-marital balance is just as much your separate property as the original amount was. It’s a detail that is frequently overlooked, leading to incorrect divisions.

The rules for this are complex, but you can learn more about how Texas courts handle community property matters here. This knowledge is absolutely vital when you're trying to figure out if the trial court made a reversible error in your case.

Understanding the Qualified Domestic Relations Order (QDRO)

When it comes to dividing a 401(k) in a divorce, one document stands above all others: the Qualified Domestic Relations Order (QDRO). This isn't just another piece of legal paperwork. It's a specialized, complex court order that acts as the bridge between your Texas divorce decree and the federal laws governing retirement plans.

If you suspect the division of your 401(k) was unfair, a flawed QDRO is often the culprit and can be a significant source of reversible error on appeal.

Think of it this way: your final divorce decree states what you're supposed to get from the 401(k). The QDRO, on the other hand, is the detailed instruction manual that tells the 401(k) plan administrator exactly how to pay you. Without a valid, judge-signed QDRO, the plan administrator is legally forbidden from giving a dime to anyone but the employee spouse. It's the QDRO that creates the legal exception for them to transfer funds to the non-employee spouse (the "alternate payee") without triggering a cascade of taxes and early withdrawal penalties.

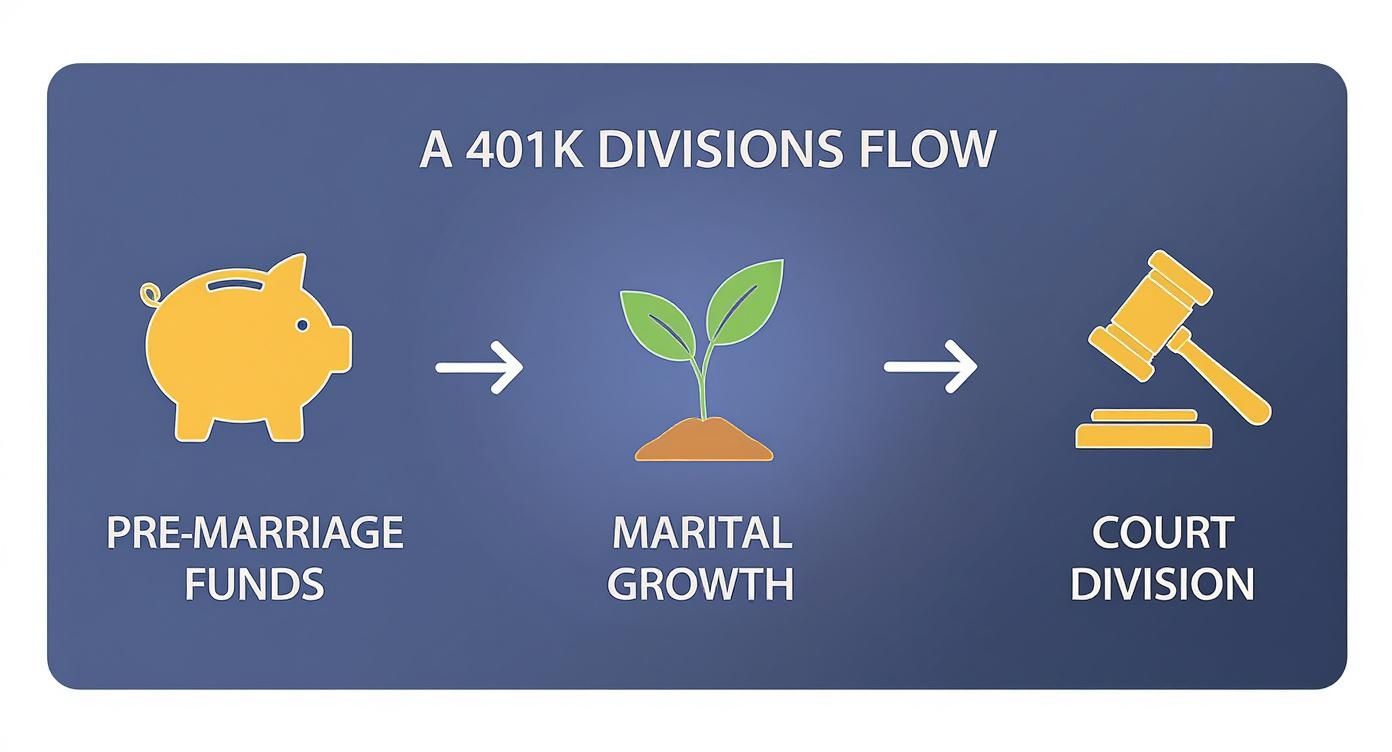

The infographic below helps visualize how this works—from identifying the marital portion of the retirement funds to the court-ordered division that the QDRO puts into action.

As you can see, only the value built up during the marriage is considered community property. That's the slice of the pie the judge divides, and the QDRO is the tool used to serve it.

The QDRO Drafting and Approval Process

Getting a QDRO finalized is a careful, step-by-step dance where every detail has to be perfect. This is not the place for a generic, fill-in-the-blank form. A single mistake can set you back months or, even worse, result in you getting less than what the judge ordered.

Here’s how the process generally unfolds:

- Drafting the Order: An attorney—ideally one with deep experience in QDROs—drafts the document. It has to include very specific information: full names and addresses, the name of the retirement plan, and the exact percentage or dollar amount being awarded.

- Getting Pre-Approval: This is a crucial, often-skipped step. Before it goes to the judge, the draft QDRO should be sent to the 401(k) plan administrator. They'll check it against their internal rules to make sure it's something they can actually execute. This prevents the nightmare of getting a judge to sign an order that the plan will just reject later.

- The Judge's Signature: Once the plan administrator gives it a preliminary thumbs-up, the QDRO is submitted to the court. The judge’s signature turns it into a binding court order.

- Final Submission: The signed order is sent back to the plan administrator for their final, official approval. Only after they formally accept it can the funds be separated and paid out.

Why Precision is Everything

A poorly written QDRO can turn a settled divorce into a financial disaster.

Let's say your decree awards you 50% of the community portion of the 401(k), valued "as of the date of divorce." If the market soars in the six months it takes to get the QDRO finalized and the order wasn't drafted to account for those gains, you could lose out on thousands. That's a clear error.

One of the most common grounds for appeal we see is a QDRO that flat-out contradicts the Final Decree of Divorce. The QDRO has to be a perfect reflection of the decree's terms. If it isn't, it creates an opening to challenge the order and fix the mistake.

Don't forget the tax implications, either. A properly executed QDRO allows the 401(k) funds to be divided without either party getting hit with immediate income taxes or the 10% early withdrawal penalty. The IRS makes this special exception, even for participants under age 59½, which is a huge financial protection for the spouse receiving the funds. You can discover more insights about 401k division rules and how this process shields your assets.

The language has to be airtight. It needs to spell out how investment gains and losses are handled between the divorce date and the payout date. It must address any outstanding loans against the account. Ambiguity is your worst enemy and a leading cause of post-divorce legal battles. If these details were missed or botched in your case, it may be a reversible error an appellate court can correct.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.

Understanding the Standard of Review for a 401(k) Division

It’s a gut-wrenching feeling to read a final divorce decree and realize the judge’s decision on your 401(k) just doesn’t line up with the facts. When a court’s ruling feels fundamentally unfair, it's easy to think there’s nothing you can do. But that’s exactly why the Texas appeals process exists—to catch and correct these kinds of judicial mistakes.

An appeal isn't a do-over of your entire trial. Instead, the appellate court takes a hard look at the existing record. An appellate attorney’s job is to comb through every piece of evidence, every testimony, and every ruling from your case to find a reversible error. This isn't just a minor mistake; it's a legal error so significant that it very likely led the trial judge to the wrong conclusion.

The "Abuse of Discretion" Standard

In Texas family law, the trial court judge has significant latitude to divide community property in a manner they deem "just and right." This legal leeway is known as judicial discretion. However, this power is not absolute. A judge commits an abuse of discretion when they act without reference to any guiding rules or principles, or when their decision is arbitrary or unreasonable.

This is the key standard of review the appellate court uses to evaluate the property division. We don't have to prove the judge was biased or had bad intentions. We just have to show that their decision was not supported by the evidence and the law. For example, awarding almost all of a large 401(k) to one spouse without a solid legal reason is a classic sign of a potential abuse of discretion.

Common Grounds for Appealing a 401(k) Division

When reviewing a case for a potential appeal, an appellate lawyer hunts for specific, critical errors that can completely change the financial outcome for a client. These are often the mistakes that form the foundation of a successful appeal.

Here are a few of the most common reversible errors:

- Mischaracterization of Property: This is a major one. If you had a 401(k) balance before you got married, that pre-marriage balance, plus any growth on it, is your separate property. If the court mistakenly lumps that in with the community funds and divides it, that's a clear legal error.

- Incorrect Valuation: A 401(k) balance can fluctuate daily with the market. If the court uses a valuation date from a year before the trial when the account was worth much less, the division can be incredibly lopsided. Just like a proper business valuation for divorce requires precision, so does valuing retirement accounts.

- A Flawed QDRO: The Qualified Domestic Relations Order (QDRO) must mirror the divorce decree perfectly. If the QDRO has a different percentage split, uses the wrong dates, or adds terms not found in the decree, it can be challenged as it does not conform to the judgment.

Imagine a real-world scenario: a spouse enters a 10-year marriage with $150,000 already in their 401(k). At the time of divorce, the court simply splits the entire final account balance 50/50 without tracing and confirming that separate property portion. That is a textbook reversible error. An appellate court can reverse that decision and remand it back to the trial court with instructions to correctly characterize the property.

The Path to Reversing an Unfair Ruling

If you suspect a serious error was made, the first step is a meticulous review of your entire case file. An appeal is not a new trial; it's a highly strategic legal argument presented in written documents called briefs. In these briefs, we pinpoint exactly where the trial judge went wrong based on the trial record and demonstrate how that mistake resulted in an unjust outcome.

Our objective is to prove to the higher court that the division wasn't "just and right" because it was built on a misapplication of Texas law. When it comes to your retirement savings, the stakes couldn't be higher. A successful appeal can be the one thing that secures the financial future you've spent your entire career building.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.

Making Smart Choices with Your Awarded 401(k) Funds

After all the legal hurdles are cleared and the QDRO is finally approved, you’re probably breathing a huge sigh of relief. But there’s one more critical decision ahead. As the "alternate payee" (the non-employee spouse), you now have to decide what to do with your awarded share of the 401(k).

This isn't just a minor detail; it’s a choice with massive, long-term financial consequences. Getting it right is crucial for building a secure foundation for your new life, so let’s walk through your options.

The Go-To Strategy: A Direct Rollover

For the vast majority of people, the smartest move is a direct rollover. This simply means you move the money from your ex-spouse's 401(k) directly into another tax-advantaged retirement account, most commonly an Individual Retirement Account (IRA) that you open and control.

Why is this the best path? Because it keeps your money sheltered from taxes. The funds roll from one retirement plan to another, and you don't owe a dime in income tax. Your money stays invested and continues to grow for your future, which is exactly where it should be.

Executing a direct rollover is the key to protecting the full value of your awarded retirement funds. It ensures your money stays invested for its intended purpose—your retirement—rather than being diminished by immediate and avoidable taxes.

An IRA also opens up a world of flexibility. Most 401(k) plans offer a pretty limited menu of investment options chosen by the employer. An IRA, on the other hand, gives you access to a much wider universe of stocks, bonds, mutual funds, and ETFs. You get to build an investment strategy that truly fits your personal goals and comfort level with risk.

The Big Mistake: Cashing Out Your Share

It can be incredibly tempting to just take the money as a lump-sum cash payment, especially when you’re facing the costs of starting over. But this is almost always a costly mistake.

The moment you choose to cash out, federal law requires the 401(k) plan administrator to withhold a mandatory 20% for federal income taxes. That money is gone before the check even gets to you.

So, if your awarded share is $100,000, you’ll only receive a check for $80,000. And that 20% is just a down payment. Depending on your total income for the year, your final tax bill could be even higher.

But the financial pain doesn't stop there. If you're under the age of 59½, the IRS will likely slap on an additional 10% early withdrawal penalty. All of a sudden, your $100,000 award has shrunk to $70,000 or even less after all the taxes and penalties.

The difference between the two choices is stark.

| Action Taken with Awarded Funds | Immediate Tax Impact | Long-Term Impact |

|---|---|---|

| Direct Rollover to an IRA | $0 in taxes and penalties. | Funds remain invested and continue to grow tax-deferred for retirement. |

| Cash Distribution | Mandatory 20% federal withholding, plus a likely 10% early withdrawal penalty. | A huge chunk of your retirement savings is lost forever, crippling your future financial security. |

Making an Informed, Strategic Decision

I get it. Sometimes cash is needed to cover immediate post-divorce expenses. But cashing out your 401(k) share should be an absolute last resort. The long-term damage to your retirement savings is almost never worth the short-term fix.

Your divorce decree and QDRO were fought for to secure a piece of that retirement pie for your future. The best way to honor that outcome is to preserve every penny by executing a direct rollover. I always recommend sitting down with a financial advisor who can provide personalized guidance to make sure your decision aligns with your new financial reality and sets you up for stability for years to come.

Common Questions on Appealing a 401k Division

When you're dealing with a divorce, the process of splitting a 401(k) can feel like navigating a maze blindfolded, and an unfair outcome only adds to the stress. Over the years, I've heard just about every question you can imagine, especially from people who feel like the initial court ruling just wasn't fair. Let's tackle some of the most common ones.

Can I Get My Share of the 401k Before the Divorce Is Final?

The short answer is a firm no. In Texas, no marital property—and that includes your share of a 401(k)—can be officially divided until the judge signs the Final Decree of Divorce. The document that actually unlocks those funds is called a Qualified Domestic Relations Order (QDRO), but even that is powerless until the divorce is finalized. A plan administrator won't even look at it until they have a signed decree and a signed QDRO in hand.

Trying to get to that money early is a big mistake. It can land you in serious legal and financial trouble. Everything has to wait for the court's final orders to be officially in place before any retirement funds can legally change hands.

How Does a 401k Loan Affect the Division?

This is a great question because an outstanding 401(k) loan absolutely complicates things. That loan balance is almost always treated as a marital debt. This means it gets subtracted from the total account value before any division happens.

Here’s a real-world example: Let’s say the 401(k) has a $100,000 balance, but there's an outstanding $20,000 loan. The actual pot of money available for division is only $80,000. The divorce decree needs to be crystal clear about how this debt is handled, and the QDRO must reflect that decision precisely. If it doesn't, the entire calculation is thrown off.

A common reversible error occurs when a trial court ignores an outstanding 401(k) loan, resulting in an inflated valuation of the community estate. This can lead to one spouse receiving a smaller share than they are entitled to, a clear basis for an appeal.

What if My Ex-Spouse Refuses to Cooperate with the QDRO?

It’s frustrating, but it happens. The good news is that the Final Decree of Divorce isn't a suggestion—it's a legally binding court order. Both you and your ex are required to follow every part of it, and that includes cooperating to get the QDRO drafted and executed.

If your ex is dragging their feet, refusing to sign paperwork, or just generally obstructing the process, you aren't stuck. You have legal options. Your attorney can file a motion to enforce the court's order, which can force your ex to cooperate. A judge can even order them to pay for the attorney's fees you had to spend just to get them to follow the rules. This is exactly why having a sharp family law or appellate attorney in your corner is so critical.

How Long Does It Take to Receive My Money After the QDRO Is Signed?

This is the part that tests everyone's patience, because the timeline can vary dramatically. Once the judge signs the QDRO, it doesn't just magically trigger a deposit into your account. The order has to be sent to the 401(k) plan administrator, who then conducts their own review for approval.

Here’s what you can generally expect:

- Best-Case Scenario: Some plan administrators are incredibly efficient. If the QDRO is drafted perfectly, they might process it within 30 to 60 days.

- More Common Reality: Frankly, it’s more likely to take several months. If the retirement plan is complex or if there are even tiny errors in the QDRO, the administrator will kick it back and ask for corrections, causing major delays.

This is precisely why getting the QDRO right the first time is non-negotiable. Any mistake or ambiguity creates delays that keep you from getting the funds you were rightfully awarded. If you suspect an error in the process has created an unjust outcome for you, it's definitely time to get a professional to evaluate your case.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.