Skip to content

Skip to content

You may feel your Texas family law case was handled unfairly, especially regarding the marital home. The final decree is supposed to create a clean break, but when it comes to a shared mortgage, you can find yourself financially chained to your ex-spouse. An unfair or poorly drafted order from the court can leave you exposed to financial risk long after the case is closed. If you believe the trial court made a significant mistake in dividing your property and debts, the Texas appeals process offers a path to seek a just outcome.

While assuming a mortgage can be a way to keep a favorable interest rate, a court order that fails to properly structure this process can be a form of reversible error.

The Financial Bind of an Unfair Post-Divorce Mortgage Order

It’s a frustratingly common scenario. The judge signs the final decree, awarding you or your ex-spouse the family home. But the court's order is vague or fails to include critical protections, leaving both of you legally bound to the mortgage lender. According to the bank, you and your ex are both still responsible for the entire debt, regardless of what the divorce decree says. This conflict between a flawed court order and your contractual obligation to the lender can leave you feeling powerless and dangerously exposed.

This gap is where the real risk lies. If the court ordered your ex-spouse to make the payments but they fall behind, your credit score takes the hit right alongside theirs. This is not just an inconvenience; it can be a direct result of a judge's failure to craft a legally sound and enforceable order—an "abuse of discretion." This type of error completely undermines the financial independence you sought in the divorce and may be grounds for an appeal. You can learn more about these financial entanglements in our guide on the cost of divorce in Texas.

Understanding Your Paths Forward After a Faulty Ruling

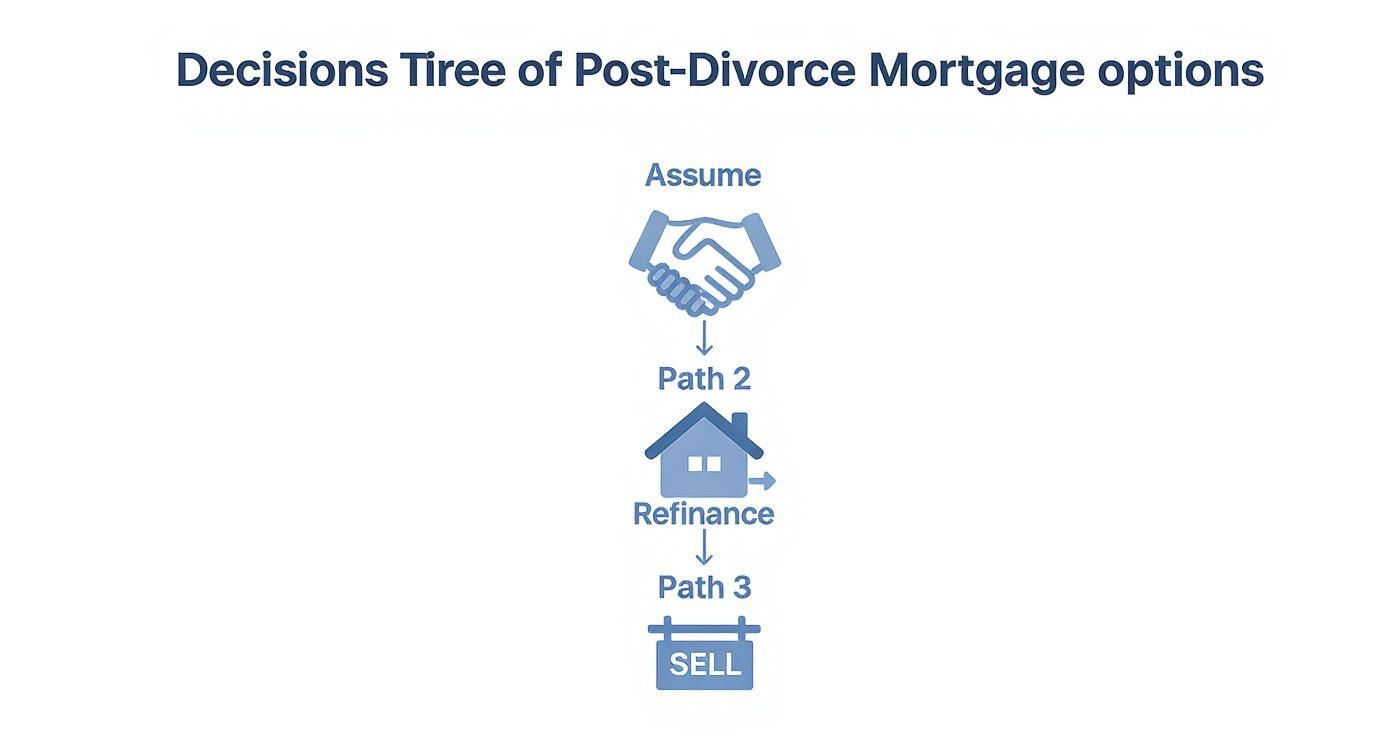

To truly untangle your finances, the court's order should have clearly mandated one of three paths. If it failed to do so, or structured the division in a way that was unjust, an appeal might be necessary to correct the error.

- Mortgage Assumption: One spouse officially takes over the existing mortgage, keeping the original loan terms. In a high-rate environment, this is a huge benefit. A court can order a party to pursue this, but it must also include enforcement mechanisms.

- Refinancing the Loan: The spouse keeping the house applies for a brand new loan in their name alone to pay off the joint mortgage. This is a common solution, but a trial court commits error if it orders a refinance without considering if the party can actually qualify on a single income.

- Selling the Home: This is often the cleanest break. The house is sold, the mortgage is paid off, and the remaining equity is split. A court's refusal to order a sale when it is the only viable option can be an abuse of discretion.

Figuring out which of these routes was appropriate and whether the trial court made a reversible error is the critical first step in an appellate review of your property division.

The decision on how to handle the marital home has profound financial and emotional consequences. An appeal is not a retrial of the facts; it is a review of the trial court's decisions to determine if a legal mistake was made that harmed you.

Let’s dig into what these options mean and how a trial court can get them wrong.

This decision tree gives a good visual overview of the main options and where they lead.

As you can see, whether you assume, refinance, or sell, each path involves unique legal and financial steps. A trial judge's failure to properly order and enforce these steps can be a basis for appeal.

What You Can Appeal in a Texas Divorce Case: Mortgage Issues

In a Texas divorce appeal, you don't re-argue your case. Instead, an appellate attorney reviews the trial record—transcripts and evidence—for "reversible error." This is a legal mistake made by the trial judge that was so significant it likely led to an unfair outcome.

When it comes to the mortgage, common reversible errors include:

- Ordering an Unrealistic Refinance: A judge ordering one spouse to refinance the mortgage without any evidence they have the financial ability to do so. This is a classic example of an "abuse of discretion."

- Failing to Include Enforcement Clauses: A decree that awards the house to one party but includes no deadlines or consequences if they fail to remove the other party from the mortgage. This leaves the departing spouse financially vulnerable and may be an improperly structured property division.

- Improper Characterization of Property: A judge incorrectly classifying separate property as community property (or vice-versa), leading to an unjust division of the home's equity.

Plain-English Definition: "Abuse of Discretion" is the primary standard of review for property division in Texas family law appeals. It means the trial court acted unreasonably, arbitrarily, or without reference to any guiding rules and principles. It's not enough that the appellate court would have decided differently; you must show the trial judge's decision was legally indefensible.

Refinancing: The Common Path Fraught with Legal Error

Refinancing is the most common method for settling a mortgage in a divorce. The spouse keeping the house gets a new loan to pay off the joint mortgage, cleanly removing the ex-spouse's name from the debt.

This creates a definitive financial split. It also allows the spouse to cash out equity to buy out the other's share, simplifying the property division.

However, a trial court can commit a reversible error by ordering a refinance that is impossible to achieve. If your joint mortgage has a 3% rate and a refinance means a 7% rate, the monthly payment could skyrocket. A judge who orders this without considering evidence of the new payment amount and the spouse's income may have abused their discretion. Getting a solid handle on your home's current value is step one; our guide on getting a home appraisal for divorce can walk you through that process.

Selling the Home: When a Court's Refusal is an Error

For many couples, selling the house is the only practical solution. It provides a clear path forward by converting the home to cash to pay off the debt and divide the remaining equity.

A court's refusal to order a sale can be an abuse of discretion if evidence shows neither party can afford to maintain or refinance the home alone. Forcing parties to remain financially entangled indefinitely is often not a "just and right" division of the community estate as required by the Texas Family Code.

Comparing Your Mortgage Options After a Texas Divorce

When you're standing at this crossroads, seeing the options side-by-side can make the right direction much clearer. This table breaks down the key benefits, challenges, and ideal scenarios for assumption, refinancing, and selling.

| Option | Key Benefit | Primary Challenge | Best For Spouse Who… |

|---|---|---|---|

| Assume the Mortgage | Keeps an existing low interest rate, saving thousands. | Must qualify for the entire loan on a single income; lender approval can be tough. | Has a low-rate, assumable loan (FHA, VA) and a strong enough financial profile to qualify alone. |

| Refinance the Loan | Provides a clean financial separation and a way to cash out equity for a buyout. | Likely means a higher interest rate and monthly payment; qualifying can be difficult. | Needs to buy out their ex's equity and can comfortably afford the new, higher payments on their own. |

| Sell the Home | Offers a complete financial break and converts home equity to cash for a fresh start. | Can be emotionally difficult; depends heavily on current market conditions. | Wants a clean slate, can't afford to keep the home alone, or needs the cash from the sale. |

Ultimately, a trial court must weigh these factors to achieve a fair outcome. If you believe the judge ignored the financial realities and made an unjust order, you may have grounds for an appeal.

How High Interest Rates Reshape Your Options

The entire conversation around mortgages and divorce has been turned on its head lately. For years, refinancing was the standard, easy answer for the spouse who wanted to keep the house. A court ordering a refinance was routine. Today, that same order can be a financial dead end, and a judge who fails to recognize this may be committing a reversible error.

The heart of the issue is simple: borrowing money has gotten a lot more expensive. Many Texas families locked in their mortgages when rates were at historic lows. Trying to qualify for a brand-new loan on a single income in this market often means staring down a much, much higher interest rate. The result? A monthly payment that can be shockingly high.

It's a painful financial squeeze. Not only are you adjusting to life on one income, but you're also up against borrowing costs that can make staying in your own home impossible. This is the kind of evidence an appellate court would review to determine if the trial judge made a fair and reasonable decision.

The New Math of Refinancing

To really see the impact, let's walk through a common scenario. Say you and your ex have a $350,000 balance on a mortgage you got back in 2021 with a great 3% interest rate. Your monthly payment for principal and interest would be right around $1,476.

Now, let's jump to the present. To get your ex-spouse's name off the loan, you have to refinance that same $350,000. But with today's rates hovering closer to 7%, your new monthly payment for the exact same debt would leap to about $2,328.

That's an $852 jump every single month. Over the course of a year, you’d be paying an extra $10,000. This "payment shock" is a critical fact. A trial court that orders a refinance while ignoring this evidence may have abused its discretion, creating grounds for an appeal.

A staggering shift has occurred in the mortgage market. Between 2021 and 2024, the average 30-year fixed mortgage rate increased from approximately 2.7% to over 7%, representing nearly a 160% increase in borrowing costs. When a spouse attempts to refinance a mortgage individually after divorce, this can increase monthly payments by 40-60% depending on market conditions and individual creditworthiness. You can find more details on how economic volatility is affecting divorces in this recent analysis.

Why a Flawed Decree Forces Your Ex to Stay on the Loan

When a court orders an impossible refinance, you end up in a legally dangerous position: your ex-spouse's name stays on the mortgage for a house they don't even live in. Your divorce decree might say you're the one responsible for the payments, but as far as the lender is concerned, you are both on the hook.

This creates serious, long-term financial risks for both of you. For the spouse who moved out, having their name tied to that old mortgage can feel like an anchor. It directly impacts their debt-to-income ratio, which can make it incredibly difficult to get a loan for a car or, more importantly, a new home of their own.

Here’s what that looks like in the real world:

- Credit Risk: If you, the one still in the house, miss a payment or pay late, it dings both of your credit scores.

- Shared Liability: In a worst-case scenario like a foreclosure, the bank can come after both of you for the debt, no matter what your divorce decree says.

- Financial Entanglement: This lingering financial connection makes a clean break impossible. It's a recipe for stress and conflict that can drag on long after the divorce is supposed to be final.

An order that creates this messy situation without a clear path to resolution is precisely the type of unfair outcome the appellate process is designed to correct.

Using Texas Law to Correct an Unfair Ruling

When you're going through a divorce, it's easy to think the Final Decree of Divorce is the last word on everything. But if that decree contains legal errors, it can be challenged. A critical detail that trips up many people is that a divorce decree cannot change the contract you both signed with your mortgage lender.

A court's failure to recognize this and include proper legal mechanisms to protect both parties can be a reversible error. An appeal seeks to have the case sent back to the trial court with instructions to fix these mistakes using specific Texas legal documents.

Without the right language in the decree, you could follow the judge’s orders perfectly and still end up on the hook for a mortgage on a house you no longer own. Fortunately, Texas law provides a clear path to secure your interests, and an appeal can force the court to use it.

The Power of Precise Language in Your Decree

Everything starts with the specific wording in your final divorce decree. Vague instructions like "Spouse A will be responsible for the mortgage" are a recipe for disaster and may constitute an abuse of discretion. A well-drafted decree is your first line of defense, and it needs to have teeth.

An appellate court will review whether the decree included a hard deadline for the other party to either refinance the loan or sell the property. For example, the language might state that your ex has 180 days from the date the divorce is final to secure a new loan.

Key Takeaway: If that deadline passes, the decree should automatically trigger a consequence, such as the immediate listing of the home for sale. The absence of such enforcement language is a common error that can be corrected on appeal.

Transferring Ownership with a Special Warranty Deed

During the divorce, you'll almost certainly sign a Special Warranty Deed. This is the legal document that officially transfers your ownership interest in the property to your ex-spouse, getting your name off the title. It's a standard and necessary step.

But this is where a huge misconception comes into play. Signing the deed does not take your name off the mortgage. The deed transfers ownership, but the mortgage is all about the debt. A court order that doesn't account for this separation between title and debt is fundamentally flawed.

Another document sometimes used is a quitclaim deed, which serves a similar purpose of transferring property interest. Just like a Special Warranty Deed, it does absolutely nothing to remove your financial obligation to the lender.

Your Ultimate Protection: The Deed of Trust to Secure Assumption

So what happens if an immediate refinance or sale isn't realistic? Texas law provides a fantastic tool called a Deed of Trust to Secure Assumption. If a trial court fails to order this protection when you are leaving the home but staying on the mortgage, it can be a reversible error. It should be signed right alongside the Special Warranty Deed.

Here’s how it works:

- It places a lien on the property in your favor.

- It legally secures the promise your ex made in the divorce decree to handle the mortgage.

- Crucially, if your ex-spouse misses payments, this document gives you the right to step in and take action—including the power to foreclose on the property yourself to make sure the lender gets paid.

This legal instrument essentially turns you, the departing spouse, into a lender with real leverage. An appeal can argue that the failure to order this document left you unfairly exposed and that the case should be remanded to include it.

Your Credit and Financial Future Are on the Line

Leaving your name on the mortgage for a house you no longer live in is one of the biggest financial gambles you can take after a divorce. An improperly drafted court order forces you into this gamble, creating a direct financial tether to your ex-spouse's reliability.

Think about it: if your ex makes even one late payment, your credit score suffers an immediate blow. This isn't just a number on a report. It's the difference between getting approved for a new car loan, qualifying for an apartment, or ever buying a home of your own again. You’re left completely vulnerable due to a court's mistake.

Don't Hope for the Best—Plan for the Worst

To sidestep this nightmare scenario, your divorce decree must contain specific, ironclad clauses. If it doesn't, an appeal is your chance to fix it. This isn't about distrust; it's about smart, protective legal strategy to correct judicial error.

A properly drafted decree should give you the power to:

- Verify payments: Include a right to receive copies of the monthly mortgage statements to confirm they're being paid on time.

- Confirm upkeep: Require your ex to provide annual proof of homeowners insurance and property tax payments.

- Set a deadline: Establish a non-negotiable date by which the house must be refinanced or sold, with clear consequences if that deadline is missed.

These provisions transform your divorce decree from a piece of paper into a powerful tool. An appeal can ensure these protections are added to safeguard your financial future.

A Hard Lesson from the 2008 Housing Crisis

The danger of this financial entanglement skyrockets during economic turmoil. We've seen it before. Past downturns show just how fast a stable situation can fall apart, trapping people in devastating financial webs.

The 2008 financial crisis is the ultimate cautionary tale. After the Lehman Brothers collapse, home values plunged by around 33% by 2012. In 2010 alone, there were a staggering 3.8 million foreclosures. Countless divorcing couples were stuck—unable to refinance, unable to sell without a massive loss, and unable to afford to live separately. When rates climb and values fall, the game changes entirely. You can dig deeper into this connection by exploring these insights on real estate debt.

The lesson here is crystal clear: never leave your financial future in someone else's hands. Proactive appellate advocacy is your only real defense against being trapped by a flawed court order.

The "Forced Sale" Clause: Your Ultimate Failsafe

One of the most critical protections a court can order is the right to force a sale of the home. If your decree lacks this clause, an appeal may be necessary. The clause is simple but powerful: if your ex fails to refinance the mortgage by the agreed-upon date, the house automatically goes on the market.

This isn't about being aggressive; it's a necessary final backstop. It guarantees that you won’t be left on the hook indefinitely for a property you don’t even own. Without it, your only option is to drag your ex back to court for a costly and exhausting enforcement lawsuit. An appeal can fix this by ensuring a mandatory sale clause is included, giving you an automatic solution that protects your credit and secures your financial freedom.

Untangling Mortgages and Divorce in Texas: Your Questions Answered

Going through a divorce is complicated enough without throwing a mortgage into the mix. If a court's decision has left you confused and financially exposed, you are right to seek answers. We get these questions all the time from clients who believe their case was decided unfairly and want to know if an appeal can help.

Let’s walk through some of the most common scenarios.

What Happens if My Ex Misses a Mortgage Payment?

This is a big one, and the answer is blunt: if your name is still on that loan, the lender holds you 100% responsible for the entire debt. It doesn't matter what your divorce decree says. A single late payment from your ex will hammer both of your credit scores.

This is exactly why a divorce decree cannot be vague. A court's failure to include iron-clad language that sets a firm deadline for your ex to either refinance or sell can be a reversible error, subject to appeal.

Can I Force a Sale if They Don't Refinance?

You absolutely can, but only if that power is spelled out in your Final Decree of Divorce. If the trial judge refused to include a "forced sale" provision despite evidence that it was necessary, this could be an abuse of discretion.

An appeal can correct this omission. A forced sale clause acts as an automatic trigger. If your ex blows past the refinancing deadline, this provision gives you the power to force the sale of the house without having to drag everyone back to court. It’s the mechanism that ensures you aren’t stuck on a loan indefinitely.

A Word of Experience: A "forced sale" clause isn't about punishing your ex. It's about creating certainty for your future. It provides a clear, enforceable consequence that an appellate court can order to be included to correct a trial court's error.

Does Signing a Deed Get Me Off the Mortgage?

No. This is probably the most dangerous misconception in divorce and real estate. Signing a Special Warranty Deed or a Quitclaim Deed transfers your ownership in the house to your ex, but it does absolutely nothing to remove your debt obligation to the bank.

Let's be clear: title (ownership) and the mortgage (debt) are two completely separate things.

Only the lender can release you from that loan. This typically only happens in one of three ways:

- Your ex-spouse refinances the loan into their name only.

- The lender formally approves a mortgage assumption during a divorce and releases you from liability in writing.

- The house is sold, and the original mortgage is paid off entirely.

A court order that fails to recognize this distinction is legally flawed and may be corrected on appeal.

What Is a Deed of Trust to Secure Assumption?

This is a uniquely powerful tool we use here in Texas. If a trial judge ordered you to move out while keeping your name on the mortgage—without the protection of a Deed of Trust to Secure Assumption—this may be a reversible error. It should be signed at the very same time you sign the deed transferring your ownership.

Essentially, this document places a lien on the property in your favor. It secures your ex's promise to pay the mortgage on time as ordered by the court. If they start missing payments, this document gives you the legal teeth to step in—up to and including the right to foreclose on them yourself—to protect your credit. It's a critical piece of leverage that an appellate court can order to ensure a fair outcome.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.