Skip to content

Skip to content

Navigating a divorce can feel overwhelming, especially when the court's decision about your family home seems unfair or financially impossible. You may feel your case was handled incorrectly, leaving you with an unworkable outcome regarding your mortgage. A divorce loan assumption is a crucial tool in Texas family law, but when a court gets it wrong, it can jeopardize your financial future.

This process allows one spouse to take over the existing mortgage, which can be a lifeline for preserving a low interest rate and providing stability. However, if the trial court’s order was based on a legal mistake, the Texas appeals process offers a path to seek a fair and just resolution.

Understanding Your Home Mortgage in a Texas Divorce Appeal

If you believe the court's decision regarding your home was unjust, you are not alone. In a Texas divorce, the home is often the most significant community asset, and the mortgage is the largest shared debt. A fair and lawful division of this asset is critical for your financial stability. An appeal is not a retrial; it is a careful review of the trial court record to determine if a reversible error occurred that led to an improper outcome.

A common issue we see is a court order that fails to properly separate the spouses' financial lives. If your name remains on a mortgage after the divorce—even if the decree makes your ex-spouse responsible for payments—your credit is at risk. A single late payment can damage your credit score and hinder your ability to secure new loans. For years, refinancing was the standard solution, but in today’s high-interest market, it is often not a viable option.

Why a Proper Loan Assumption Order is Crucial

This is precisely why a correctly structured divorce loan assumption is so vital. Instead of obtaining a new, more expensive loan, one spouse can take over the original mortgage, preserving its favorable terms and interest rate.

This isn't a minor detail; it impacts a significant number of Texans. A 2022 report highlighted that about 53.4% of American couples going through a divorce owned a home together, placing the mortgage at the center of property division. You can explore more about these financial trends from Roth Capital Partners.

A fair property division must be grounded in a realistic financial plan. An assumption can preserve a low-interest mortgage, providing stability and preventing the forced sale of the family home.

An essential step in this process is determining the home's value through a professional home appraisal for divorce. If a trial court’s order overlooks practical solutions like loan assumption, mischaracterizes property, or makes a legal mistake in dividing your assets, the appeals process exists to help you seek a just and workable outcome.

What You Can Appeal in a Texas Divorce Loan Assumption Case

When you’re facing the aftermath of a divorce trial, legal terms can be confusing. One of the most important concepts in appellate law is reversible error. This isn't just a minor mistake; it's a significant legal error made by the trial judge that likely led to an unfair judgment. A divorce loan assumption order can contain several types of reversible errors.

The goal of an assumption is to allow one spouse to keep the family home without the burden of refinancing. It's like taking over a lease—you step into the existing contract with its original terms and interest rate. This can provide immense financial relief, but only if the court's order is legally sound and protects both parties.

Understanding the Standard of Review

On appeal, a higher court reviews the trial judge's decisions using a specific legal standard. For property division, that standard is typically abuse of discretion.

- Abuse of Discretion (Plain English Definition): This means the trial judge made a decision that was arbitrary, unreasonable, or without reference to any guiding legal rules or principles. For example, ordering a spouse with insufficient income to assume a mortgage, knowing it would be impossible for them to qualify, could be an abuse of discretion.

The appellate court examines the trial record—transcripts and evidence—to see if such an error occurred.

- The Assuming Spouse: This is the party ordered to take full responsibility for the mortgage. The court must consider whether they have the financial capacity to do so.

- The Releasing Spouse: This is the party moving out, who must be fully released from the mortgage obligation to achieve a clean financial break.

The most critical element for the releasing spouse is securing a "release of liability" from the lender. This document formally confirms they are no longer legally tied to the mortgage debt.

A verbal promise from your ex or even a judge's order in the divorce decree isn't enough. Only a formal release of liability from the bank truly severs that financial tie and protects your credit if your ex misses a payment down the road.

If a court’s final order fails to ensure this release is obtainable, it can be a significant reversible error. A flawed order that creates an unjust property division can be challenged on appeal, restoring balance and fairness.

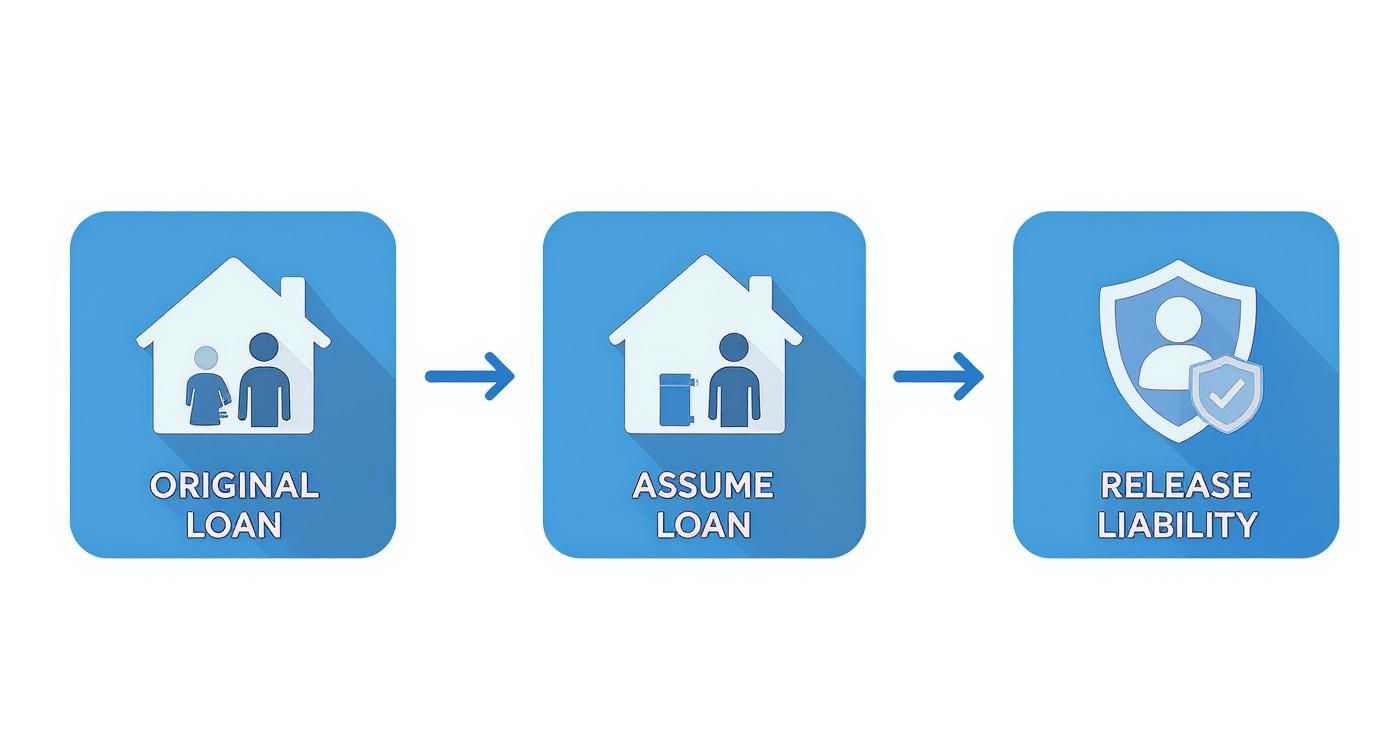

The Step-by-Step Texas Loan Assumption Process

The loan assumption process in a Texas divorce is a sequence of legal and financial steps that demand precision. The foundation for a successful assumption is the Final Decree of Divorce. An appellate attorney will scrutinize this document for errors. It must contain clear, unambiguous language that awards the home to one spouse and mandates the complete removal of the other spouse from all liability. Vague language is a common source of reversible error.

Securing the Property Transfer: A Point of Potential Error

After the decree is signed, legal documents must be filed to execute the property transfer. An error in this stage can invalidate the court’s intent.

Two documents are essential:

- Special Warranty Deed: This document officially transfers ownership. When signed by the departing spouse and filed, the assuming spouse becomes the sole legal owner.

- Deed of Trust to Secure Assumption: This acts as a crucial safety net. It places a lien on the property, giving the departing spouse the right to foreclose if the assumption is not completed by the court-ordered deadline.

The goal is to transition from a shared financial burden to a clean separation of assets and liabilities.

This process is designed to result in a formal release of liability for the departing spouse. If the court's orders make any step impossible, it may be grounds for appeal.

The Lender's Approval Process and Due Process

With the legal paperwork in place, the assuming spouse must apply to the lender. Under a federal law called the Garn-St. Germain Act, lenders generally cannot accelerate a loan due to a transfer in a divorce. This act provides the legal framework for a divorce loan assumption.

However, approval is not guaranteed. The lender will conduct a full financial review of the assuming spouse, examining:

- Sufficient Income: Proof of ability to handle payments alone.

- Credit Score: A history of responsible borrowing.

- Debt-to-Income Ratio: A measure of total monthly debt versus income.

After approving the assumption, the lender issues the "Release of Liability" to the departing spouse. This is the final step that severs their financial connection to the mortgage. If a judge's property division order creates an impossible standard for one spouse to meet, effectively denying them due process, it could be a reversible error subject to appeal.

Loan Assumption vs. Refinancing in a Divorce

Understanding the difference between these two options is crucial, as a court's failure to consider the most just and equitable path could be an abuse of discretion.

| Feature | Loan Assumption | Refinancing |

|---|---|---|

| The Loan | Keeps the original mortgage loan intact. The terms, interest rate, and payment schedule do not change. | Pays off the old loan and replaces it with a brand-new loan with new terms, a new rate, and a new payment. |

| Interest Rate | Preserves the existing interest rate, which is a huge benefit if the original rate is low. | You get the current market interest rate, which could be higher or lower than your original rate. |

| Closing Costs | Generally lower. Involves processing and administrative fees but avoids many typical closing costs. | Involves full closing costs, including appraisal, title, and origination fees, which can be 2-5% of the loan. |

| Equity Payout | Does not provide a way to pull cash out of the home's equity to pay the other spouse. | A "cash-out" refinance allows you to borrow against the equity to pay the other spouse their share. |

| Best For… | Couples who have a great interest rate they want to keep and don't need to pull cash out of the home's equity. | Couples who need to buy out the other spouse's equity or who can secure a better interest rate than the old one. |

An appeal can argue that the trial court ordered a financially detrimental path (e.g., a forced refinance into a high-rate loan) when a more equitable option like assumption was available and feasible.

Common Reversible Errors in Loan Assumption Orders

When evaluating your case for an appeal, our attorneys look for specific legal mistakes. A divorce loan assumption order can be a source of significant error if it creates an unfair or unworkable outcome. The goal of an appeal is to identify these mistakes and seek a judgment that is fair, lawful, and practical.

An incorrect ruling can harm both parties. The assuming spouse may be trapped with an impossible financial burden, while the releasing spouse may remain tied to a debt they no longer control.

Examples of Reversible Errors

Here are some common legal errors we analyze in divorce appeals involving property division:

- Ordering an Impossible Act: A judge commits an abuse of discretion by ordering a spouse to assume a mortgage when evidence shows they cannot possibly qualify based on their income and credit. This sets the party up for failure and financial ruin.

- Failing to Secure the Releasing Spouse: A decree is legally flawed if it transfers the house but fails to include provisions ensuring the departing spouse receives a "Release of Liability" from the lender. This improperly leaves them financially exposed. The frequency of these issues is significant, considering there were roughly 2.3 divorces per 1,000 people in the U.S. in 2020 alone. You can find more global divorce statistics on Divorce.com to see how common these situations are.

- Ignoring a More Equitable Solution: If evidence supported a loan assumption that would preserve a low interest rate, but the court instead ordered a costly and unnecessary sale of the home or a refinance, this could be challenged as an abuse of discretion.

The single greatest risk for the departing spouse is failing to get a formal "Release of Liability" from the lender. Without that piece of paper, you are still legally on the hook for the mortgage. Your credit score is completely tied to whether your ex makes their payments on time.

If your divorce decree contains a vague or impossible order regarding your mortgage, this could be the reversible error needed for a successful appeal. An experienced appellate attorney can evaluate your case to determine if a legal mistake compromised your financial future and whether an appeal is the right path to correct it.

What to Do When a Loan Assumption Is Not an Option

Sometimes, a divorce loan assumption is simply not feasible. The lender may deny the application, or the original loan terms may not permit it. If the trial court failed to consider these realities and did not provide a workable alternative, its judgment may be flawed.

When assumption is off the table, the court must still craft a fair and equitable division. A judgment that fails to do so may be challenged on appeal.

Exploring Your Alternatives

A trial court has several tools to divide property when assumption is not possible. A failure to properly use these tools can constitute an abuse of discretion.

Here are common alternatives that should be considered:

- Sell the Home: This provides the cleanest financial break by paying off the mortgage and allowing for the division of remaining equity.

- Use an Owelty Lien: This legal tool allows one spouse to buy out the other's equity interest. It is often paired with a refinance, but the court must ensure the refinancing spouse can actually qualify.

- Arrange Temporary Co-Ownership: The parties might be ordered to co-own the home for a specific period. A sound order will include detailed provisions for mortgage payments, maintenance, and the conditions for a future sale. A vague co-ownership order is often legally insufficient.

An unworkable court order that forces you into a financially impossible situation could be the basis for an appeal. A fair property division must be grounded in reality, and if the judge's order ignored practical alternatives, it may be considered an abuse of discretion.

While divorce rates in the United States have declined by 42.5% over the last 20 years, the financial complexity of each case has only grown. You can read more about these demographic trends on Rayden Solicitors.

If you believe the court’s decision was legally flawed because it ignored these real-world financial constraints, an appellate attorney can help you understand your rights. Learn more about how we handle complex property division appeals.

Appealing an Unfair Ruling on Your Marital Home

If the trial court's final order regarding your home and mortgage is unjust or legally flawed, the Texas appellate process provides a remedy. For example, if the court ordered a divorce loan assumption knowing the lender would never approve it, leaving you in financial limbo, you have the right to seek justice.

An appeal is not a second trial or an opportunity to present new evidence. It is a methodical review of the trial court record. Our appellate attorneys analyze every transcript, exhibit, and ruling to identify a reversible error—a legal mistake so critical that it likely caused an improper judgment. The process involves extensive legal research and writing, culminating in a formal document called a brief.

- Briefing (Plain English Definition): This is the process of writing and submitting a formal legal argument to the appellate court. The brief explains what legal errors the trial judge made, cites relevant laws and past cases, and argues why the decision should be overturned.

Understanding Grounds for an Appeal

You cannot appeal a judgment simply because you are unhappy with the outcome. The appeal must be based on specific legal errors.

Common reversible errors in property division cases include:

- Abuse of Discretion: The judge's decision was arbitrary or unreasonable. For example, ordering a spouse with no income and poor credit to assume a mortgage is a classic example of an unworkable and thus unreasonable order.

- Misapplication of the Law: The court incorrectly applied Texas law, such as mischaracterizing separate property (like an inheritance) as community property and dividing it.

- Legally Flawed Orders: The divorce decree is defective if it orders one spouse off the deed but lacks the necessary language to ensure a "release of liability" for the mortgage, leaving them legally responsible for a debt on a home they no longer own.

An appeal is your opportunity to correct legal mistakes and seek a truly just and right division of your property, as required by the Texas Family Code. It ensures that the final order is not just a decision, but a fair and legally sound resolution.

If the trial court's order has placed your financial security in jeopardy, you have the right to have a higher court review that decision. By identifying these kinds of errors, an appeal can be a powerful tool for correcting an unjust result. For more information on this process, explore our resources on divorce order appeals.

Diving Deeper: Your Questions About Divorce Loan Assumptions Answered

When a divorce loan assumption is part of your case, specific questions and concerns are common. Clear, accurate answers are vital for protecting your rights, whether during trial or on appeal.

Will Assuming the Loan Hurt My Credit Score?

This depends on your role.

For the spouse keeping the home, taking on the full mortgage will increase your debt-to-income ratio, a key factor in your credit score. However, making timely payments on your own will build a strong, positive credit history.

For the spouse leaving the home, obtaining a formal "release of liability" from the lender is non-negotiable. Without it, the mortgage remains on your credit report. Any late payments by your ex-spouse will damage your score. A court order that fails to facilitate this release may be considered reversible error.

What if My Ex-Spouse Refuses to Cooperate?

A divorce decree is a binding court order. If it requires your ex-spouse to cooperate with the assumption process and they refuse, you can file a motion to enforce the order. A judge can compel them to sign the necessary documents. An appellate court can review whether the original decree was sufficiently clear and enforceable to protect your rights.

Are All Mortgages Assumable in a Divorce?

Most government-backed loans (FHA, VA, USDA) are assumable.

Conventional loans typically contain a "due-on-sale" clause. However, federal law provides a critical protection in divorce cases.

The Garn-St. Germain Act creates a special exception for property transfers that happen because of a divorce. This powerful act stops the lender from calling the loan due just because the home's title was transferred from one spouse to the other.

An appellate review would examine whether the trial court correctly considered the nature of the loan and the applicability of federal law when making its orders.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.