If you are facing a divorce, the process of dividing complex assets like a 401(k) can feel overwhelming and unjust. You may feel your case was handled unfairly, especially when a significant portion of your retirement savings—funds you worked years to accumulate—was awarded to your ex-spouse. In Texas, community property laws mean that retirement funds earned during the marriage are subject to division, but this division must be legally sound and equitable.

When a trial court makes a mistake in characterizing or valuing these critical assets, the financial outcome can be devastating. An unjust ruling, however, does not have to be the final word. The Texas appellate process exists to correct legal errors and ensure that the division of your property is truly "just and right" under the law.

How a 401k Should Be Divided in a Texas Divorce

When a Texas judge evaluates a 401(k) for property division, their duty is to order a "just and right" division of the community portion of the account. This does not automatically mean a 50/50 split. It requires a meticulous process: identifying funds earned during the marriage, valuing them correctly, and carefully separating them from any funds that qualify as separate property.

It is a common and legitimate concern to feel that your years of financial contribution have been disregarded or that a court's decision is fundamentally unfair. This often occurs when complex financial assets are at stake. An unjust ruling, however, is not the end of the road. The appellate process is designed specifically to review and correct legal mistakes made by trial courts.

Understanding the Standard of Review for a 401k Division

Because Texas is a community property state, the law presumes that most assets acquired during the marriage should be divided equally. However, for a 401(k), the analysis is more nuanced. Only the contributions—and the growth on those contributions—that occurred during the marriage are subject to division.

Any funds you had in the account before the marriage are your separate property, but the law requires you to prove this with clear and convincing evidence. This is where errors often occur. For example, a court might use an outdated valuation method or fail to account for the passive growth on your separate property funds. This misapplication of the Texas Family Code can lead to a profoundly unfair division and is a common basis for a successful appeal.

Dividing retirement accounts is just one piece of the puzzle. For a broader look at the financial side of a split, this guide on finance and divorce offers some really helpful context.

To help you get a handle on the terminology, here are some of the key terms you’ll encounter.

Key Legal Terms in a Texas 401k Divorce Split

This table breaks down essential legal concepts into plain English, so you can understand the principles involved in appealing the division of your retirement accounts.

| Term | Plain-English Definition |

|---|---|

| Community Property | Any asset, including 401(k) contributions and earnings, acquired by either spouse during the marriage. |

| Separate Property | Assets owned by a spouse before marriage, or received during marriage as a gift or inheritance. This includes the 401(k) balance before the wedding. |

| Reversible Error | A significant legal mistake made by the trial court that likely caused an improper judgment and can be corrected on appeal. |

| Qualified Domestic Relations Order (QDRO) | A special court order required to divide a retirement plan without tax penalties. A divorce decree alone is not sufficient. |

| Abuse of Discretion | The legal standard for most family law appeals. It means the trial judge made a decision that was arbitrary, unreasonable, or without a basis in law or fact. |

| Briefing | The process of writing and submitting formal legal arguments to the appellate court, explaining why the trial court's decision was wrong. |

Understanding these terms is the first step toward protecting your rights and seeking a just and fair division of your assets.

What You Can Appeal in a 401k Divorce Split

It is critical to understand that an appeal is not a second trial. You cannot re-argue the same facts or introduce new evidence. An appeal is a formal review of the trial record to determine if the court made a significant legal mistake, which is known as a reversible error.

In a 401k divorce split, common reversible errors that we look for include:

- Mischaracterization of Property: This is a major error. It occurs when the court incorrectly treats separate property (like your pre-marital 401(k) balance and its growth) as community property subject to division.

- Valuation Errors: Using an incorrect date to value the account or applying a flawed formula can dramatically alter the outcome and lead to an unjust division.

- Unequal Division Without Justification: A judge may order an unequal division, but they must state a legally sound reason on the record. Punishing one spouse without legal justification is not a valid reason.

If you believe an error like this occurred in your case, our appellate attorneys can meticulously review the trial record—the official account of what happened in court—to determine if there was an abuse of discretion. To learn more, take a look at our detailed guide on splitting a 401k in a divorce.

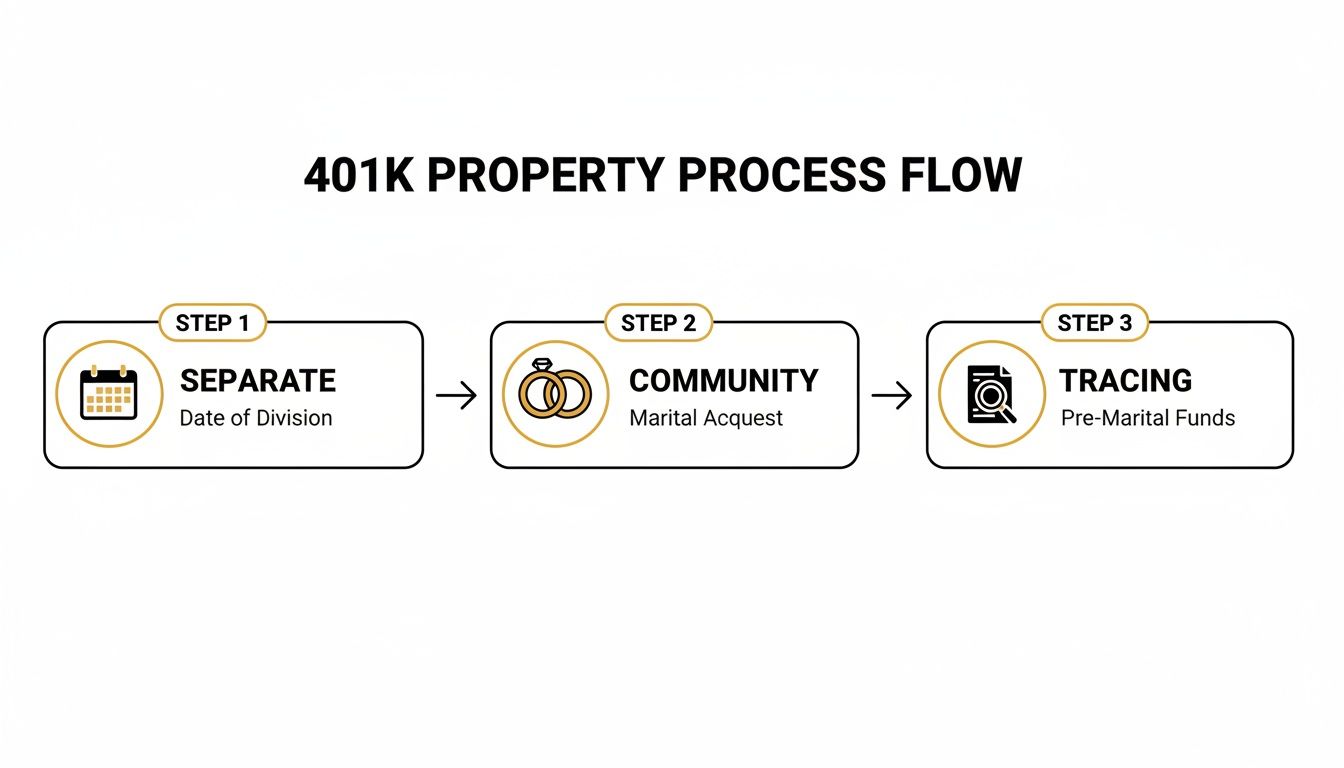

Figuring Out What’s Yours, Mine, and Ours in a 401(k)

When people feel their financial outcome in a divorce was unfair, it almost always boils down to one thing: how the property was classified. In a Texas divorce, getting a handle on the difference between community property and separate property inside your 401(k) is absolutely critical. This isn't just about splitting an account down the middle; it's about protecting the retirement funds you earned and owned long before you ever said "I do."

The starting point in Texas is simple. By law, everything you and your spouse acquired from the date of marriage to the date of divorce is presumed to be part of the community estate. For your 401(k), that means every dollar you or your employer contributed—plus all the investment gains on those dollars—during the marriage is considered community property.

The Uphill Battle: Proving Your Separate Property

So, what about the money you had in that 401(k) before you got married? That’s your separate property. Here’s the catch, though: the burden is on you to prove it.

You have to provide "clear and convincing evidence" to trace those pre-marriage funds. If you can't, the judge has no choice but to treat the entire account as community property and divide it. This is where things can go sideways, fast.

A simple tracing error or missing statement can lead to a huge financial hit, and it’s often a solid reason for a property division appeal. The court has to get the law right, and ignoring properly traced separate property is a classic example of reversible error.

To have any shot at proving your claim, you'll need to get your hands on some very specific documents:

- The Pre-Marriage Statement: This is the big one. You need the account statement from right around your wedding date to establish the starting balance of your separate property.

- Statements During the Marriage: You'll need a full history to show how the separate and community funds grew over the years. This isn't always easy to get, but it's necessary.

- The Divorce-Date Statement: This statement shows the final account value that the court will be dividing.

How Tracing Works in the Real World

Let's walk through a common scenario. Say you had $50,000 in your 401(k) when you got married. Fifteen years later, after consistent contributions and market growth, the account is now worth $400,000.

It would be a major legal mistake to just subtract your initial $50,000 and call the remaining $350,000 community property. Why? Because your original funds grew, too.

Key Takeaway: The investment growth on your initial $50,000 is also your separate property. An expert, usually a forensic accountant, needs to run the numbers to figure out how much of the total growth came from your separate funds versus how much came from the new community contributions.

Failing to account for the passive growth on separate property is an all-too-common mistake in trial courts. It's a misapplication of Texas law that ends up handing a chunk of your separate assets to your ex-spouse. When this happens, it’s considered an abuse of discretion by the judge. A sharp appellate lawyer can pinpoint this mistake and argue to a higher court that the property division was fundamentally unjust.

For a deeper dive into these foundational rules, you can read more about how Texas community property state laws work in our detailed guide. Correctly identifying and proving your separate property isn't just a legal technicality—it's the most important step in securing a fair division of your retirement.

If you believe the court got it wrong and mischaracterized your 401(k), you might have a strong case for an appeal. A successful appeal can fix the error and restore the assets you worked so hard to build.

How a Qualified Domestic Relations Order (QDRO) Really Works

So, you have a divorce decree in hand that says how your 401(k) is supposed to be split. You might think that's the end of it, but it’s really just the beginning. That decree, on its own, has no power to actually move a single dollar from a retirement account.

To do that, you need a second, highly specialized court order called a Qualified Domestic Relations Order, or QDRO for short. Think of it this way: your divorce decree is the general agreement, but the QDRO is the specific, official instruction manual you hand directly to the 401(k) plan administrator.

This isn't just a piece of procedural red tape; it's a non-negotiable requirement under federal law. A QDRO is the only way to execute a 401(k) divorce split without getting slammed with a massive tax bill and early withdrawal penalties. Without a properly executed QDRO, the retirement funds are legally stuck, leaving everyone in a frustrating state of financial limbo.

Before you can even get to drafting a QDRO, you first have to figure out what part of the 401(k) is actually on the table for division.

As you can see, properly tracing and identifying the separate and community property portions of the account is the essential groundwork. Get this part wrong, and the whole division can be unfair from the start.

The QDRO Drafting and Approval Gauntlet

Getting a QDRO from draft to final approval is a meticulous, multi-step process that can trip up even experienced professionals. It starts with drafting the order, but here’s the catch: there is no universal template.

Every single retirement plan has its own unique rulebook for what it will and won't accept in a QDRO. Using generic, vague language is a one-way ticket to rejection by the plan administrator, which means more delays, more legal fees, and more headaches.

Here’s a pro tip that can save you months of frustration: get it pre-approved. Before the QDRO is ever sent to the judge for a signature, a draft should be sent directly to the 401(k) plan administrator. They will review it and tell you exactly what needs to be changed to meet their strict requirements. This simple step is one of the most effective ways to avoid a painful cycle of rejection and revision.

Why Every Word in a QDRO Matters

The devil is truly in the details when it comes to QDRO language. The order must be crystal clear and leave absolutely no room for interpretation.

A compliant QDRO must specify:

- The exact, full name of the retirement plan.

- The names and last known mailing addresses for both the plan participant and the "alternate payee" (the ex-spouse receiving the funds).

- The precise dollar amount or percentage of the benefits to be paid out.

- The time period or number of payments the order covers.

Even a seemingly minor error can derail the whole thing. For instance, if the QDRO specifies a division date that falls on a weekend or a market holiday, the plan administrator may reject it outright. This is precisely why it's critical to work with an attorney who is fluent in both Texas family law and the intricate rules governing retirement plans.

A word of warning: one of the most common—and devastating—mistakes is delaying the QDRO process. If the spouse with the 401(k) dies, retires, or takes out a loan against the account before the QDRO is finalized and approved, the other spouse’s share could be reduced or lost entirely. Time is of the essence.

The Real-World Consequences of a Flawed QDRO

When a QDRO is drafted incorrectly, or worse, never completed, the financial fallout can be severe. The funds legally remain with the original account holder, and the spouse who was supposed to receive a share has no enforceable claim with the plan.

This often means heading back to court for expensive enforcement actions. A properly executed QDRO is the key to splitting a 401(k) without triggering income taxes or the dreaded 10% early withdrawal penalty for anyone under age 59½. Remember, every single 401(k) or pension plan requires its own distinct QDRO. This is different from IRAs, which can be divided using a simpler "transfer incident to divorce."

Failure to finalize a QDRO means the account isn't divided, period—no matter what your divorce decree says. In Texas, courts can review these property divisions for an abuse of discretion, like when an asset swap doesn't account for the tax-deferred status of a 401(k). You can learn more about how retirement accounts are divided in a divorce to understand these crucial differences.

If you suspect the court made a significant error in your property division or that the QDRO process was fundamentally mishandled, it could be grounds for an appeal. An appellate court can review the case to determine if the trial court’s orders were legally sound and resulted in a just and right division of your marital estate.

Common Reversible Errors in a 401k Divorce Split

You might walk away from your divorce feeling the judge’s decision on your 401(k) was just plain wrong. But in the world of appeals, a gut feeling of unfairness won’t get you very far. An appeal isn’t a do-over of your trial; it’s a laser-focused review to see if the trial judge made a specific legal mistake.

When it comes to a 401(k) divorce split, these mistakes are called reversible errors, and they can have a massive impact on your financial future. An appellate attorney's job is to comb through the trial record—every transcript, every exhibit—looking for those critical missteps where the judge either misinterpreted Texas law or made a ruling that was arbitrary and unsupported by the evidence. This is the essence of appellate advocacy: ensuring the law was followed correctly.

Mischaracterizing Separate Property as Community Property

This is one of the most common and costly reversible errors in Texas family law. It happens when a judge treats your separate property as if it were community property, putting a portion of your non-marital retirement funds on the chopping block.

For instance, a judge might simply take the 401(k) value at the time of divorce and subtract the value on the date of marriage. This shortcut completely ignores all the passive growth that your pre-marriage balance earned over the years, which is also your separate property. If you presented clear evidence tracing that separate property growth and the court disregarded it, you have a classic reversible error.

Using the Wrong Valuation Date

In the world of retirement accounts, timing is everything. A 401(k) can gain or lose thousands of dollars in a matter of weeks depending on the market. That's why Texas law is clear: assets should be valued on or very near the date of divorce.

Picture this: the court values your 401(k) using a statement from six months before your trial. In the meantime, the market took off. Using that old, lower number means your ex-spouse gets a smaller piece of a now much larger pie. On the flip side, if the market crashed, using an old, inflated number could mean you owe them more than is fair. A judge using an outdated or random valuation date without a solid legal reason is a mistake that can absolutely be appealed.

Ordering an Unequal Division Without Just Cause

Texas is a community property state, and while a 50/50 split is the norm, it's not a strict requirement. A judge can order an unequal division, but—and this is a big but—they have to have a legally recognized reason for doing so. They can’t just wing it.

Legally valid reasons for an unequal split might include:

- Fault in the breakup of the marriage (like adultery or cruelty)

- A significant difference in earning capacity between the spouses

- One spouse deliberately wasting community assets

A judge cannot order a 60/40 split simply because they felt sorry for one person or thought the other "deserved" less. They must state their specific reasons on the record. If there’s no legally valid reason given for a disproportionate division, that decision constitutes an abuse of discretion.

An appeal isn't about re-litigating who was right or wrong. It's about questioning the how and why behind the judge's final order to ensure it was reached through a legally sound process.

What Is "Abuse of Discretion?"

This is the key legal standard in Texas family law appeals. An abuse of discretion occurs when a trial judge makes a decision without any basis in the law or the facts—in other words, acting arbitrarily or unreasonably. The question for the appellate court is not whether they would have decided the case differently, but whether the trial judge’s decision was so far outside the bounds of acceptable legal judgment that it must be corrected.

Proving an abuse of discretion requires a meticulous analysis of the entire trial record and persuasive legal briefing. Our role is to build a compelling argument showing the higher court not only that a legal mistake was made, but that this specific mistake likely led to an improper final judgment. A flawed ruling from the trial court does not have to be the end of the story for your financial security.

Considering Strategic Alternatives to a 401(k) Split

While a QDRO is the most common way to handle a 401(k) in a divorce, it's not your only option. In fact, physically splitting the account isn't required, and sometimes a more creative solution ends up being a much better financial move for both parties. The most frequent alternative we see is what's known as an "offset."

The idea is pretty simple. Instead of dividing the retirement plan, one spouse keeps their entire 401(k) untouched. To make things fair, the other spouse gets community assets of equal value. This might mean taking a larger slice of the equity in the family home, keeping a whole brokerage account, or receiving a rental property.

This kind of trade can be very attractive, especially if one person has a strong emotional attachment to the house or if selling off other assets would be a logistical or financial nightmare. But you have to be careful here, because not all dollars are the same.

Understanding the Tax Implications of an Offset

The biggest tripwire in an offset is taxes. A 401(k) is funded with pre-tax money, meaning the IRS hasn't taken its cut yet. When you pull that money out in retirement, every single dollar is taxed as ordinary income.

On the other hand, the equity in your home or the cash in your savings account is post-tax. You've already paid taxes on that money. This is the crucial difference: a dollar inside a 401(k) is not worth the same as a dollar in your hand.

It's a fundamental mistake for a court to approve a dollar-for-dollar swap of pre-tax retirement funds for post-tax assets. For instance, trading $100,000 from a 401(k) for $100,000 in home equity is not an equitable trade. That $100,000 in the 401(k) might only be worth $75,000 (or even less) after taxes are finally paid, depending on your tax bracket down the road.

This kind of unequal division is a textbook valuation error and can be a strong basis for an appeal. A "just and right" division under Texas law requires the court to look at the real-world value of assets, and that absolutely includes the tax consequences.

When Does an Offset Make Financial Sense?

When handled correctly, an offset can be an incredibly useful strategy. The secret is making sure the asset values are properly adjusted to reflect their true, after-tax worth before any trade is made.

Here are a few situations where an offset might be the smart play:

- Avoiding Market Volatility: Splitting a 401(k) means selling off investments. If the market is down, that can lock in serious losses. An offset lets the account owner ride out the storm without selling.

- Simplifying the Process: For smaller 401(k)s, the legal fees and hassle of drafting and processing a QDRO can sometimes outweigh the benefit of the split itself.

- Keeping Specific Assets: If one spouse desperately wants to stay in the family home, especially to provide stability for the kids, trading away their interest in a 401(k) can be the key to making that happen.

- Liquidity Needs: The spouse receiving the offset gets immediate access to assets (like cash or home equity), whereas money from a 401(k) rollover is still locked up for retirement.

Ultimately, choosing between a 401(k) divorce split and an offset comes down to running the numbers with a clear-eyed financial analysis. If a court overlooks the tax impact and awards a lopsided property division, it may have abused its discretion—and that's exactly what appeals are for. A fair result isn't about the number on the account statement; it's about what that money is actually worth in the real world.

Protecting Your Retirement During and After Your Divorce

Getting through a divorce is a marathon, not a sprint. The same is true for protecting your financial future. You’ve worked hard to build your retirement savings, and it takes a smart, proactive approach to keep those assets safe from common mistakes both during and after the legal process.

If you suspect an error has already been made in your property division, it's important to know that an unfair outcome isn’t necessarily the final word. The Texas appellate process is there to fix legal mistakes, but your first and best line of defense is taking the right steps from the start.

Your Pre-Divorce Action Plan

Before the ink is dry on the final decree, your focus should be on gathering facts and understanding the rules of the road. Getting organized now is the single best way to avoid the kinds of costly errors that can lead to a difficult appeal later on.

- Round Up All Financial Documents: Start collecting 401(k) statements immediately. You’ll need records from before the marriage, throughout the marriage, and right up to the present day. These documents are the foundation for tracing any separate property claims.

- Get Your Plan's Specific Rules: Every 401(k) plan operates a little differently. Contact the plan administrator and ask for their QDRO procedures and the summary plan description. Knowing their exact requirements is non-negotiable.

- Talk to a Financial Advisor: Your lawyer handles the legal side, but a financial pro can run the numbers. They can show you how different division scenarios will play out over the long term and impact your retirement goals.

It's also a good idea to get a handle on the broader tax implications of major life changes like divorce, as this will affect your entire financial situation.

Critical Post-Divorce Steps

Once the judge signs the divorce decree, the work isn't finished. There are a few more crucial steps to take to finalize the 401k divorce split and secure your financial future.

Key Takeaway: The most urgent post-divorce task is getting the QDRO finalized. It needs to be drafted, signed by the judge, and formally approved by the plan administrator as soon as possible. Your divorce decree alone won't divide the account, and any delay is a huge risk. If your ex-spouse retires, dies, or borrows from the plan first, you could lose everything.

Don't forget to update your beneficiary designations on all of your financial accounts, not just the 401(k) in question. If you skip this, your ex-spouse could end up inheriting your retirement funds when you pass away, no matter what your will or divorce decree says. The plan administrator has to follow the beneficiary form they have on file, period.

Finally, if you believe the court got it wrong with the division of your retirement, you have to act fast. Strict deadlines under the Texas Rules of Appellate Procedure apply. A timely appeal can correct issues like a mischaracterization of property or a valuation error, helping you secure the fair outcome you are entitled to.

Common Questions We Hear About 401(k) Division in Texas Divorce

When you're dealing with the financial fallout of a divorce, especially concerning retirement funds, a lot of specific questions come up. If you're worried that the division of your 401(k) wasn't fair, getting straight answers is the first step. Here are some of the most pressing concerns we hear from clients who are thinking about appealing their case.

How Much of My 401(k) Does My Spouse Actually Get?

In Texas, the court only divides the community property portion of your 401(k). This means everything that was contributed—plus all the investment gains and losses—from the day you got married until the day you got divorced is on the table.

What isn't? Any money you had in the account before the marriage. That, along with the growth on those specific pre-marriage funds, is considered your separate property. The catch is, the burden of proof is on you to prove it with clear and convincing evidence, usually in the form of old financial statements.

What if I Can't Find My Old 401(k) Statements?

This happens more often than you'd think, and frankly, it can be a huge problem. If you can't track down the statements needed to prove your separate property claim (the one from right around your wedding date is the most critical), the court has to assume the entire account is community property.

This can be a massive financial hit and underscores just how vital it is to keep good records. Without that paper trail, your separate property can easily get lumped into the marital estate and split.

Can We Just Agree to Split It and Skip the QDRO?

Absolutely not. While a handshake agreement might seem simpler, it won't work for a 401(k). The divorce decree itself doesn't have the power to move retirement funds. You need a Qualified Domestic Relations Order (QDRO), which is a separate, specialized court order.

Federal law requires a QDRO. Without one, the plan administrator is legally prohibited from transferring any money to your ex-spouse. Trying to withdraw the funds yourself to pay them can trigger massive tax bills and early withdrawal penalties. It's a mandatory step.

What Happens if My Ex Dies Before the QDRO is Done?

This is a terrifying and time-sensitive scenario. If your ex-spouse, the one whose name is on the 401(k), passes away before the QDRO is drafted, signed by the judge, and officially approved by the plan administrator, you could lose everything.

In that situation, the plan’s beneficiary designation—which may or may not name you—will likely control who gets the money. This is precisely why getting the QDRO finalized immediately after the divorce is non-negotiable.

Can I Appeal if the Judge Ignored My Separate Property Proof?

Yes, and this is a solid reason for an appeal. If you laid out clear, convincing evidence tracing your separate property and the court still wrongly classified it as community property, that's what we call a reversible error.

This is a classic example of an abuse of discretion. It means the judge didn't apply Texas law correctly, which led to a property division that was anything but "just and right." An appellate court has the power to step in and fix that mistake.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation at https://familylawcourtappeals.com.