Skip to content

Skip to content

You may feel your case was handled unfairly after your Texas divorce was finalized, especially when it comes to the marital home. If you're the one keeping the house, "assuming the mortgage" is an option that comes up often. It essentially means you're stepping into the existing home loan, taking over the payments, the interest rate, and all the original terms, while getting your ex-spouse's name—and their liability—off the books for good.

This is just one of the paths you can take, but a court order that ignores your financial reality can feel unjust. Let's break down what you need to know about this process and how to seek a fair outcome if you believe the court made a mistake.

Your First Steps with the Marital Home After Divorce

It’s an overwhelming feeling when a judge's order about your home just doesn't seem fair or, worse, financially possible. You might be staring at a divorce decree that leaves you financially tethered to your ex-spouse, creating a messy and uncertain future. The first thing you need to understand is the crucial difference between being on the deed versus being on the mortgage.

In Texas, the deed is about ownership, while the mortgage is about the debt. A common reversible error we see is when a divorce decree awards the house to one spouse (via a deed transfer) but fails to address removing the other spouse from the mortgage. This is a nightmare scenario for the person who moved out. They're still legally on the hook for a massive debt on a house they don't even own, which can wreck their credit and block them from getting new loans.

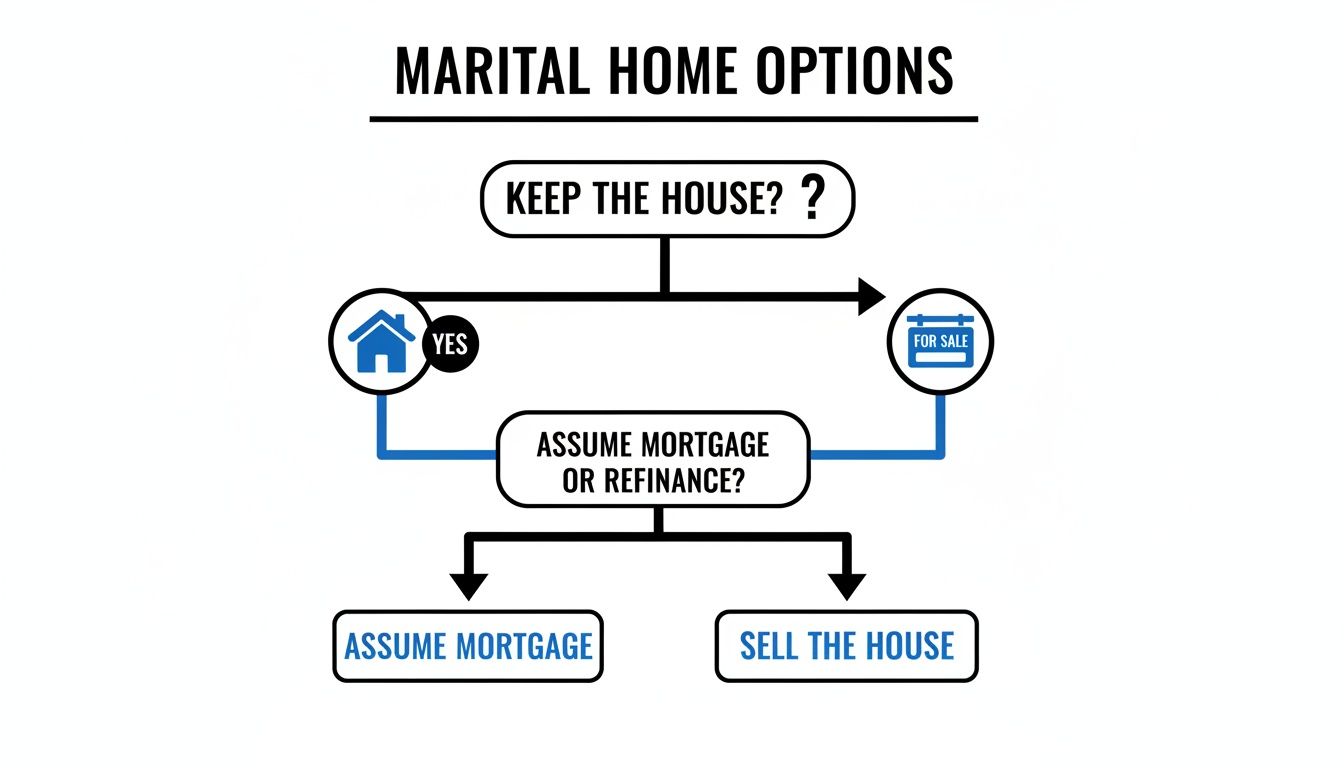

To avoid that outcome, you have three main options for the house.

Understanding Your Three Core Options

Your final divorce decree needs to spell out exactly which path you and your ex are taking. Each one has its own set of rules and will shape your financial life for years to come.

- Mortgage Assumption: This is where you formally take over the existing loan. The biggest perk? You get to keep that original interest rate, which is a huge win if you locked in a low rate years ago. The catch is that the lender has to approve you based on your income alone. Not all loans are assumable, but federal law does offer some key protections for transfers that happen because of a divorce.

- Refinancing: You get a brand-new loan in your name only, and that money pays off the old joint mortgage. This creates a clean financial break, which is great. The downside is you have to qualify for this new loan at today's interest rates, and if they've gone up, your monthly payment could jump significantly.

- Selling the Property: Sometimes, the cleanest break is the best one. You both agree to sell the house and split the profit as the court orders. This is often the most straightforward solution, especially if neither of you can comfortably afford the home on a single income.

This chart lays out the fork in the road you'll face.

As you can see, the first decision is whether to keep the house. If the answer is yes, that's when you have to dig into the details of an assumption versus a refinance.

Comparing Your Options For The Marital Home After Divorce

This table breaks down the three primary pathways for handling the mortgage on the marital home after a Texas divorce, helping you understand the pros, cons, and typical requirements for each.

| Option | Key Requirement | Best For | Potential Pitfall |

|---|---|---|---|

| Mortgage Assumption | Lender approval based on your sole income and credit; loan must be assumable. | Spouses who want to keep a low, existing interest rate and can qualify for the loan on their own. | Lender denial; not all loan types (especially conventional) are assumable. |

| Refinancing | Qualifying for a brand new mortgage based on current rates, your income, and credit. | Creating a clean financial break when the original loan has a high rate or isn't assumable. | Higher interest rates can lead to a much larger monthly payment; closing costs. |

| Selling the Home | Mutual agreement to sell and a clear plan for dividing the equity. | Couples who want to completely sever financial ties or when neither spouse can afford to keep the home. | A slow real estate market; disagreements over the sale price or division of proceeds. |

Choosing the right path depends entirely on your financial situation, the terms of your current mortgage, and what you and your ex-spouse can agree on.

Understanding the Standard of Review

If your divorce decree is vague or poorly drafted when it comes to the house, you're setting yourself up for serious legal and financial headaches down the road. An ambiguous order can leave you exposed if your ex fails to make payments or drag their feet on a required refinance.

One of the most common reversible errors we see in Texas family law is a judge ordering a property division that simply isn't feasible. Forcing a spouse to take on a home they can't possibly qualify for on their own is often considered an "abuse of discretion" and can be grounds for an appeal.

If the court’s final order is unworkable, it might be what lawyers call a reversible error. In plain English, a reversible error is a legal mistake made by the trial judge that likely caused an improper outcome. An appellate court can review the trial record—everything said and submitted in your original case—to see if the judge's decision was fair and just based on the facts presented. The best defense is a good offense: understanding your options from the start allows you to fight for a fair and, most importantly, enforceable property division agreement.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.

Mortgage Assumption vs. Refinancing in Texas

When the marital home is on the line, figuring out your finances is the first step toward genuine independence after a divorce. You really have two main roads you can go down: mortgage assumption or refinancing. They might sound similar, but they're fundamentally different and will have a massive impact on your financial future.

With a mortgage assumption, you're formally asking the lender to transfer the existing home loan—with its original interest rate and terms—into your name only. Refinancing, on the other hand, means you get a brand-new loan in just your name to pay off and completely close out the old joint mortgage.

The Core Difference Explained

Here's a simple way to think about it: assuming a mortgage is like taking over someone's car lease. You inherit the exact same payments and terms. Refinancing is like trading that car in for a new one, complete with a fresh financing agreement based on whatever the market looks like today.

The choice between the two often comes down to one thing: the interest rate. If you locked in a fantastic low rate years ago, holding onto it through an assumption could save you thousands of dollars. It can be the one thing that makes keeping the house affordable on a single income.

In the U.S., about 65-70% of the nearly 830,400 divorces each year involve real estate. That’s over 581,000 cases where couples have to make tough decisions about their home. A classic, devastating mistake is when one spouse removes the other from the deed but then gets denied for a refinance. This leaves the ex who moved out still legally on the hook for the mortgage debt but with zero ownership—a true financial nightmare.

What Is a Due-on-Sale Clause?

As you dig in, you’ll definitely come across the term "due-on-sale clause." This is standard language in most mortgage contracts saying the loan must be paid in full if the property is sold or transferred. At first glance, it sounds like a deal-breaker for assumption.

But there's a critical federal law that helps: the Garn-St. Germain Depository Institutions Act of 1982. This law specifically stops lenders from activating the due-on-sale clause when a property transfer happens because of a divorce decree. This protection is what legally opens the door for you to assume a conventional mortgage after divorce, if you can meet the lender’s other financial requirements.

This legal protection is a powerful tool, but it's not a free pass. The lender still gets to vet your financial stability. You have to prove you can handle the payments on your own before they'll agree to formally release your ex-spouse from the loan.

Real-World Scenario: Assumption vs. Refinancing

Let’s look at a real-world example. Imagine a divorcing couple has a $300,000 balance on their mortgage with a great 3% interest rate. Their monthly principal and interest payment is about $1,265.

- Assumption Path: The spouse who wants to keep the house applies to assume the loan. If approved, they just keep paying the $1,265 a month. That low rate is preserved, and their housing costs stay predictable.

- Refinancing Path: Now, let's say they have to refinance. The spouse must qualify for a new $300,000 loan. If today's interest rates are hovering around 7%, the new monthly payment would jump to roughly $1,996. That's an extra $700 coming out of their budget every single month.

This stark difference is why assumption is so attractive right now. However, refinancing does offer a cleaner break and gives you the option to pull out equity to buy out your ex-spouse's share of the home, which isn't possible with a simple assumption. If you're exploring that route, a guide on refinancing your mortgage to consolidate debt can offer some valuable perspective.

Ultimately, picking the right path demands a hard look at your specific loan type, your personal finances, and the precise wording in your divorce decree. A poorly written order that doesn't account for these financial realities can be a disaster and may even be grounds for an appeal.

Navigating the Lender Approval Process

Winning the house in a divorce decree is one thing. Convincing the bank you can actually afford it on your own is an entirely different battle, and it's often the biggest hurdle you'll face. The court order gives you the right to the property, but the lender needs proof you can carry the financial weight solo.

You have to go into this with a solid strategy. The last thing you want is to finalize the divorce only to find out you can't get the financing, putting the house—and your stability—at risk. The lender is about to put your financial life under a microscope, and you need to be ready for the scrutiny.

Getting Your Financial Ducks in a Row

Before you even pick up the phone to call the lender, your first job is to gather your financial paperwork. Think of it as building your case. Showing up organized and prepared sends a strong signal that you're a responsible borrower who takes this seriously.

A complete and tidy package can make the difference between a quick approval and a drawn-out, painful process. Using a thorough mortgage documentation checklist is a great way to ensure you haven't missed anything. At a minimum, be ready to hand over:

- Proof of Income: Have your last two years of tax returns, W-2s or 1099s, and at least a month's worth of recent pay stubs ready to go.

- Asset Verification: Lenders need to see where you stand. Gather statements from all your accounts—checking, savings, retirement, and any investments—to show you have cash reserves.

- Credit Report: The bank will pull your full credit report, but you should already know what’s on it. They'll be looking at your score, payment history, and any outstanding debts.

- Final Decree of Divorce: This is non-negotiable. It’s the legal proof that the court has awarded you the property and ordered the mortgage transfer.

Can You Use Support Payments to Qualify?

For many newly single spouses, demonstrating enough income is a major stress point. This is where spousal or child support payments become absolutely critical. The good news is that lenders will count this as qualifying income, but they are incredibly strict about the proof.

You can't just say, "I get $1,500 a month." You must provide the Final Decree of Divorce where the payment amount and duration are clearly spelled out. Even more importantly, you’ll have to prove you’ve been receiving it consistently. That means showing bank statements with deposits for at least the last three to six months.

Lenders perform a financial "stress test" to gauge your long-term ability to make payments. They need to see a stable and reliable income stream, which is why a consistent history of receiving court-ordered support payments on time is so important for your application's success.

This is a make-or-break detail. If your ex-spouse has been late or inconsistent with payments, it could torpedo your application before it even gets started. It’s a harsh reality that underscores why enforcing court orders is so important. For a deeper look into these financial hurdles, you can explore the specifics of the divorce loan assumption process.

The All-Important Debt-to-Income Ratio

When it comes down to it, one number matters more than almost any other to a lender: your debt-to-income (DTI) ratio. It’s a simple calculation that compares your total monthly debt payments—mortgage, car loans, credit cards, everything—to your gross monthly income.

As a general rule, most lenders want to see a DTI of 43% or lower. Some might be more flexible if you have a great credit score or significant cash reserves, but 43% is the magic number to aim for.

To figure out your DTI, just add up all your monthly debt obligations and divide that total by your pre-tax monthly income. For instance, if your gross income is $6,000 a month and your total debts (including the new mortgage payment) add up to $2,400, your DTI is 40% ($2,400 ÷ $6,000).

Knowing this number before you apply gives you a realistic snapshot of your approval chances. If it's too high, you know you need to pay down some debt before approaching the bank. If the judge's final order saddles you with a DTI that makes it impossible to qualify, that could be a red flag pointing to a fundamentally unfair property division that may need a second look from a legal expert.

Getting the Language Right in Your Divorce Decree

Your Final Decree of Divorce is much more than a piece of paper—it's your legal shield. When dealing with the house, the specific words used in this document can be the difference between a clean financial break and a years-long, expensive headache with your ex. A vague or poorly written decree is one of the most common and damaging mistakes, leaving one spouse completely vulnerable.

To protect yourself, the decree has to be airtight and enforceable. It can’t leave any room for excuses or delays. This is the document you'll hand a judge if your ex doesn't hold up their end of the bargain, so its clarity is absolutely critical for your financial future.

Must-Have Clauses to Protect Yourself

Your decree needs to do more than just say who gets the house. It has to order specific actions, set firm deadlines, and spell out what happens if those orders are ignored. Think of it as a detailed set of instructions that a court can enforce without a second thought.

To make sure your decree has real teeth, insist on these critical elements:

- A Hard Deadline: The decree needs a specific date by which your ex must either assume the mortgage or get a new loan. Vague language like "in a reasonable time" is a recipe for disaster. A concrete deadline, like 90 or 180 days from the day the divorce is final, creates a clear, non-negotiable obligation.

- A "What If" Clause: What happens if the deadline comes and goes? The decree must state the penalty. This is your safety net. Often, this clause requires the house to be immediately listed for sale if the refinance or assumption isn't completed on time.

- Who Pays for What: The order should explicitly name the person responsible for the mortgage payments, property taxes, and homeowner's insurance until the loan is officially out of the other's name. This eliminates any arguments over who owes what during that transitional period.

Without these details, you could easily end up back in court filing an enforcement action, which is a drain on your time, money, and emotional well-being.

Understanding the Key Texas Legal Documents

Here in Texas, the divorce decree alone isn't enough to get the job done. You need specific legal documents drafted and signed to actually carry out what the judge ordered. Knowing what these documents are is essential to securing your financial independence.

A shockingly common and reversible error in Texas family law cases is when a decree fails to include language for a Deed of Trust to Secure Assumption. This mistake leaves the departing spouse on the hook if the other defaults, creating a deeply unfair result that can often be fixed on appeal.

Two documents are absolutely vital:

- Special Warranty Deed: This is the document that officially transfers title. It takes the property out of both your names and puts it solely in the name of the spouse who is keeping the house. It's how you get your ex's name off the deed.

- Deed of Trust to Secure Assumption: This might be the single most important document for the spouse moving out. It creates a lien on the property that secures the promise to pay the mortgage. If the spouse in the house fails to make payments, this document gives the other spouse the power to step in, foreclose, and force a sale to pay off the mortgage, saving their credit from ruin.

The relationship between the divorce decree and these deeds is complex, and a mistake can have devastating consequences. If you're dealing with the fallout from a poorly drafted order, understanding the proper process for assuming a mortgage after divorce is the first step toward finding a fair solution.

When the Judge Gets It Wrong: Spotting Errors for an Appeal

You may feel your case was handled unfairly if the judge signs a final order that forces you to assume a mortgage you know you cannot qualify for. This can leave you feeling trapped by a court order that seems completely unworkable, putting your financial future at risk.

This is exactly why the Texas appellate process exists. It’s not about getting a "do-over" just because you don't like the outcome. It's a critical safety valve designed to correct significant legal mistakes and ensure the property division is truly "just and right" as required by the Texas Family Code.

When a trial court’s decision is fundamentally unfair or legally incorrect, it likely contains what we call a reversible error. This isn't just a minor disagreement; it's a specific legal blunder that, had it not occurred, would have probably led to a different, more equitable result.

What is an "Abuse of Discretion"?

Family court judges in Texas have a lot of leeway—or discretion—when it comes to dividing community property. But that power isn't absolute. An appellate court can, and will, step in if it finds an abuse of discretion.

So what does that mean in plain English? An abuse of discretion happens when a judge makes a ruling that is arbitrary, totally unreasonable, or goes against established legal rules. It’s a decision that falls so far outside the bounds of what’s considered fair that it demands correction.

Let's say you presented bank statements, pay stubs, and a lender's pre-qualification letter all showing it’s impossible for you to assume the mortgage. If the judge ignores all that evidence and orders you to do it anyway, that’s a textbook example of abusing their discretion. The order is impossible to follow from day one and essentially sets you up to fail.

Common Reversible Errors in Property Division Cases

When a mortgage assumption is part of a divorce decree, certain mistakes frequently pave the way for a successful appeal. A seasoned appellate lawyer will dig through every piece of the trial record—the hearing transcripts, the submitted evidence, the final order—searching for these critical missteps.

Here are some of the most common reversible errors in Texas family courts:

- Ignoring Financial Reality: The court awards the house to one spouse despite clear evidence they can't qualify for the mortgage, resulting in a decree that can never be enforced.

- Refusing to Order a Sale: When it's obvious neither person can afford the home on their own, the only fair solution is to sell it and split the proceeds. A judge’s stubborn refusal to order a sale can be an abuse of discretion.

- Mischaracterizing the Property: The judge incorrectly labels a home owned before the marriage (separate property) as community property, leading to a wildly skewed and unfair division.

- Using Bad Numbers: Relying on an old or inaccurate home appraisal can throw the entire property division off balance, giving one spouse a financial windfall at the other's expense.

One of the most financially devastating issues is the failure to secure refinancing post-divorce. The spouse keeping the house often can't qualify alone, leaving the other spouse trapped on a loan for a house they no longer own. This hits women especially hard; research shows their household income drops by 41% after divorce, compared to just 21% for men, making an impossible mortgage assumption even more crushing. In Texas, these situations often point back to trial court errors that are ripe for correction on appeal.

How an Appeal Differs From a Trial

It's vital to understand that an appeal is not a new trial. You don't get to introduce new evidence or call new witnesses.

Instead, your appellate attorney builds a powerful legal argument, known as a brief. In this document, they meticulously point out to the higher court where and how the trial judge made a legal error, using only the evidence and testimony from the original case. The entire goal is to prove that the judge's decision on the mortgage wasn't just a bad call, but a legally flawed one.

If the court of appeals agrees, it can reverse the trial court's order and send the case back down with specific instructions for a new, legally sound ruling. This could mean ordering the house to be sold or forcing a complete re-evaluation of the entire property division. You can learn more about the specific grounds for an appeal in a civil case to see how this works in practice.

If you believe the court’s order in your divorce is unworkable and unjust, don't assume it's the final word. Our appellate attorneys can review your case to see if a legal error gives you grounds to seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.

What If the Court's Decision Feels Wrong? An Appellate Attorney Can Help

It’s a deeply unsettling feeling—walking out of court knowing the judge made a critical mistake with your home and finances. But that decision doesn't have to be the final word. For many, this is where the real fight for a just outcome begins.

The Texas appellate process is specifically designed to be a check on the trial court, a way to correct legal errors that can have devastating financial consequences. This includes major missteps in how property, like your marital home and its mortgage, is divided.

Finding the Path to a Fairer Outcome

If the property division in your divorce feels fundamentally unfair—maybe the judge ordered a mortgage assumption that’s financially impossible for you to handle, or completely ignored key evidence—it’s not something you just have to live with.

Our appellate attorneys specialize in digging into the court record with a fine-tooth comb. We're looking for what are known as reversible errors, like a clear abuse of the court's discretion, and then we build a powerful, persuasive case to present to the higher court. Your financial future is simply too important to leave in the hands of a flawed ruling when there are clear legal remedies available.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.

Unpacking Common Questions About Divorce and Mortgages

Going through a divorce brings up a ton of financial questions, and the house is usually at the top of the list. It's a huge asset and a huge debt, so it's natural to feel overwhelmed. Let's tackle some of the most common worries that come up when you're trying to figure out a mortgage after a Texas divorce.

What Happens If My Ex Misses the Refinance Deadline?

This is a scenario that plays out far too often. If your ex-spouse blows past the court-ordered deadline to refinance or assume the mortgage, your divorce decree is your first line of defense. A well-written decree won't just ask them to refinance; it will command it and spell out exactly what happens if they don't.

Typically, the consequence is that the house must be immediately listed for sale. This isn’t a suggestion—it's a court order. You can take your ex back to court by filing an enforcement action. A judge can hold them in contempt for ignoring the decree, which could mean fines or even jail time. This is precisely why getting the language in your decree right from the start is non-negotiable.

Can a Judge Really Force Me to Take on a Mortgage I Can't Afford?

No. A Texas court’s job under the Texas Family Code is to divide your community estate in a "just and right" manner. Forcing you to take on a mortgage payment you've proven you can't handle would be the opposite of that. In legal terms, it could be considered an abuse of discretion.

This is a huge deal and could be a key point for a successful appeal. If you're in this situation, you have to show the trial court clear-cut evidence of your income, your other debts, and your inability to qualify for the loan on your own. If a judge ignores that evidence and orders you to take on the house anyway, it's time to call an appellate attorney. They can spot this kind of reversible error and fight to get it corrected.

A court order that’s impossible to follow from day one isn't a "just and right" division of property. It's a setup for failure, and an appellate court focused on fairness and due process may see it that way, too.

How Long Will It Take to Assume or Refinance the Mortgage?

Patience is key here, as these things never move as fast as you'd like. The timeline really depends on the lender and how complicated your own finances are. Under the Texas Rules of Appellate Procedure, timelines are strict, but the mortgage process itself has its own pace.

Here’s a realistic ballpark:

- Mortgage Assumption: You’re usually looking at 60 to 90 days from the time you turn in all the required paperwork.

- Refinancing: A standard refi tends to be a bit quicker, often closing in about 45 to 60 days.

That said, always plan for hiccups. Lenders can be slow, and unexpected issues can pop up. Your divorce decree should set a reasonable but firm deadline—something like 90 to 180 days post-divorce—to give your ex enough time to get it done without letting it drag on forever.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.