Skip to content

Skip to content

You may feel your case was handled unfairly after your Texas divorce is finalized, especially when it comes to the house and mortgage. If a judge ordered a mortgage arrangement that seems unjust or financially impossible, it's easy to feel powerless. This is a common and stressful situation, but an unfair ruling from a trial court does not have to be the final word. When one spouse is ordered to keep the home, an assumption of mortgage after divorce is a key step, and errors in how the court handled it can be grounds for an appeal.

An assumption allows one spouse to formally take over the entire mortgage, preserving the original interest rate and terms. However, if the court's order regarding the assumption, refinancing, or division of property was based on a legal mistake, you have the right to seek justice through the appeals process. Understanding your appellate options is the first step toward correcting an unfair outcome and restoring financial balance.

What You Can Appeal in a Texas Divorce Case

Many Texans walk away from their divorce feeling the court’s decisions about their home and mortgage were fundamentally unfair. It's a vulnerable position, especially if a judge ordered your ex-spouse to handle the mortgage payments, yet your name remains on the loan.

A common and dangerous misconception is that a divorce decree automatically protects you. The hard reality is that your divorce decree is an order between you and your ex-spouse; it does not alter the contract you both signed with the mortgage lender. Until that lender formally releases you from the loan, your credit score is at risk if your ex-spouse misses a payment.

The Two Main Paths for Separating a Mortgage

To truly sever the financial ties to a marital home, Texas law provides two primary options. Errors in how a trial court ordered these options can often form the basis of an appeal.

- Mortgage Assumption: One spouse formally takes over the existing mortgage, keeping the original loan terms and interest rate. The assuming spouse must qualify for the loan based on their sole income and credit, a fact that trial courts sometimes overlook, creating a reversible error.

- Refinancing: The spouse keeping the home gets a new loan in their name only to pay off the original joint mortgage. The challenge here is that the new loan will be at current interest rates, which could lead to a much higher payment. An order to refinance may be an abuse of discretion if evidence showed the spouse could not qualify.

Dividing jointly owned property can be complex, and mistakes happen. It is critical to understand the difference between separate and community property. You can learn more by exploring our guide on commingling in real estate to see how these rules might affect your case.

Navigating these paths is challenging. This table breaks down the key differences.

Mortgage Assumption vs. Refinancing At a Glance

| Feature | Mortgage Assumption | Refinancing |

|---|---|---|

| Interest Rate | Keeps the original, often lower, interest rate. | Gets a new loan at current market rates, which may be higher. |

| Loan Terms | The original loan's terms (length, type) remain unchanged. | A completely new loan is created with new terms. |

| Closing Costs | Generally lower fees, as it's not a new loan. | Involves standard closing costs for a new mortgage. |

| Qualification | The assuming spouse must qualify based on their sole income. | The refinancing spouse must qualify for a brand-new loan. |

| Lender Approval | The original lender must approve the assumption. | Any lender can be used for the new refinance loan. |

| Best For | Keeping a great interest rate and predictable payments. | When assumption isn't an option or you want to cash out equity. |

Both options aim to get one name off the mortgage. The "best" choice depends on interest rates, finances, and lender approval.

Remember this critical point: A Texas divorce decree cannot, on its own, remove a name from a mortgage. Only the lender can grant a "release of liability" through an approved assumption or refinance. This is the only way to achieve financial independence.

If you feel the trial court's property division created an impossible financial burden, it may be the result of a legal error. If a judge made a mistake known as an abuse of discretion—a legal term meaning the decision was unreasonable or without regard for the facts or law—you could have grounds for an appeal. An appellate attorney can review your case to identify such errors and seek a fairer outcome.

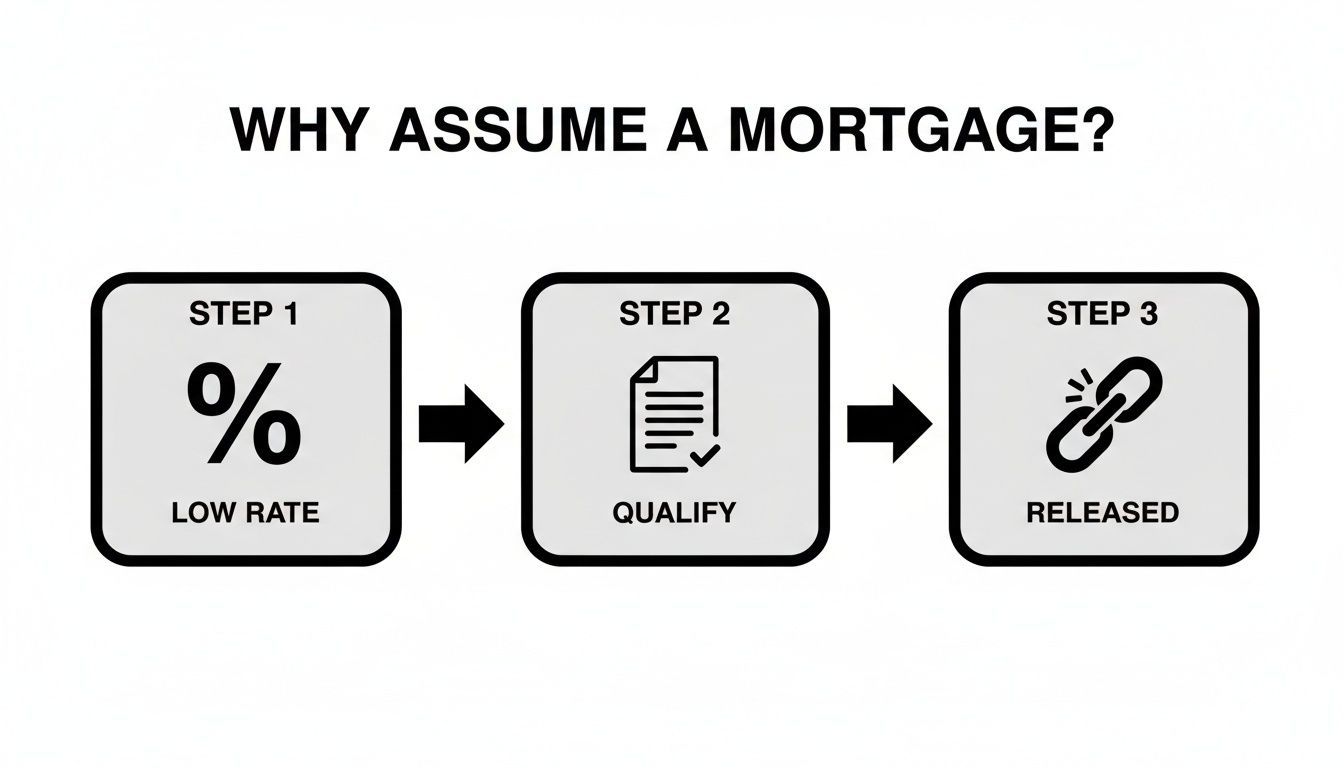

Why a Mortgage Assumption Could Be Your Smartest Financial Move

Untangling finances after a divorce requires strategic decisions. A mortgage assumption allows one spouse to take over the existing home loan, keeping the original terms—including a low interest rate locked in years ago. In today's market, that can be a game-changer.

For example, a mortgage secured a few years ago at 3.5% is far more affordable than one refinanced today at 6.5% or higher. That difference could add hundreds of dollars to the monthly payment, making a home unaffordable.

Understanding the Standard of Review in Property Appeals

The beauty of an assumption is preserving that low interest rate, which provides financial stability. By taking over the existing loan, you avoid the shock of current market rates. The financial impact is significant. On a $500,000, 30-year mortgage at 3.50%, the monthly payment is around $2,245. Refinancing at 6.75% would increase the payment to about $3,242—a nearly $1,000 monthly increase. You can review the legal analysis on mortgage assumption and divorce for more details.

But is Your Loan Even Assumable?

This is the first question to answer. The loan type determines whether it can be assumed.

-

Government-Backed Loans: Mortgages from the FHA, VA, or USDA are almost always assumable. The assuming spouse must prove they can qualify financially on their own.

-

Conventional Loans: Most conventional loans contain a "due-on-sale" clause. However, a federal law, the Garn-St. Germain Depository Institutions Act of 1982, creates an exception for transfers related to a divorce. This Act prevents the lender from calling the loan due simply because the title was transferred to an ex-spouse.

Thanks to this federal protection, your ex-spouse should be allowed to assume the loan, provided they can demonstrate the income and credit to handle the payments alone.

Key Takeaway: The Garn-St. Germain Act prevents lenders from blocking a mortgage assumption simply because the property changed hands in a divorce. The lender must allow the assumption if the spouse qualifies.

The Most Important Step: The Release of Liability

A common mistake is believing a deed transfer is enough. A deed only transfers property ownership; it does not remove a name from the mortgage contract. You remain legally responsible.

The only way to officially sever your financial obligation is to get a release of liability from the lender. This document is the final step in a successful assumption. Without it, if your ex-spouse misses a payment, your credit score is damaged, and the bank can pursue you for the money.

While assumption is often the best path, the benefits of refinancing a home loan may sometimes make more sense. If your original divorce decree created an unworkable financial situation around the mortgage, it might be grounds for an appeal. A flawed order that ignores a spouse’s inability to assume or refinance could be deemed an abuse of discretion by the court—a type of reversible error our appellate team is trained to identify.

The Texas Mortgage Assumption Process Explained

A divorce decree ordering one spouse to take over a mortgage is just the starting point. The decree provides the legal authority, but the real work involves dealing with the lender and specific legal documents. Following this process precisely is crucial to protecting your financial future.

First, provide a certified copy of your divorce decree to the mortgage lender. This proves a judge has ordered one spouse to take sole responsibility. The lender will then provide an assumption package, which is essentially a new loan application.

The process offers significant benefits: locking in a low rate, qualifying on your own, and finally, releasing the other person from the debt.

Step-by-Step Insights on Texas Appellate Procedure

Once the assumption process begins, the lender will conduct a thorough financial review of the assuming spouse. This underwriting is mandatory to ensure they can handle the mortgage payments alone.

Be prepared to provide a complete financial picture, including:

- Proof of Income: Recent pay stubs, W-2s, and the last two years of tax returns.

- Asset Verification: Bank statements and details of retirement or investment accounts.

- Credit Report: The lender will pull a new credit report.

- Debt-to-Income (DTI) Analysis: A calculation of monthly debts versus gross monthly income.

Lenders need certainty that the person assuming the loan is a safe financial bet. Any delays can halt the entire process.

Executing Key Legal Documents

In addition to the lender’s requirements, several critical Texas legal documents must be executed.

A Special Warranty Deed legally transfers the home's title from both spouses to the one keeping it. Once signed, it is filed with county property records to create a public record of the new ownership.

Next, the lender requires a Deed of Trust to Secure Assumption. This document legally binds the assuming spouse to the terms of the original mortgage note, making them the sole responsible borrower.

Crucial Insight: A deed alone is not enough. A Special Warranty Deed transfers ownership but does not remove the departing spouse's name from the mortgage. Only the lender's official "Release of Liability" can accomplish that.

Finally, upon approval, the lender issues the Release of Liability. This document is the most important for the departing spouse, as it officially and permanently removes them from any future mortgage obligation. Without it, the process is incomplete.

Sometimes, mortgage issues stem from errors in the original trial. If the court’s property division was based on a flawed home appraisal for divorce, it could have led to an unfair order. A significant valuation mistake can be a reversible error, providing grounds to appeal for a just and right division of property.

What to Do When Your Ex Won't Follow the Decree

It is incredibly frustrating when your ex-spouse ignores a court order to get your name off the mortgage. This inaction leaves your name tied to a massive debt and puts your credit score in jeopardy.

A Texas divorce decree is a binding court order. When your ex-spouse ignores it, they are violating a judge's command, and Texas law provides a remedy.

Your Next Step: A Motion for Enforcement

The most direct way to compel compliance is by filing a Motion for Enforcement in the same court that handled your divorce. This motion formally notifies the judge that your ex-spouse is not following the order.

Filing the motion initiates a new legal process. The court will schedule a hearing where you can present evidence of non-compliance. A judge has significant power to enforce their orders.

- Compelling Action: The judge can issue a new order with a firm deadline for your ex-spouse to complete the assumption or refinancing.

- Forcing a Sale: If your ex-spouse cannot or will not secure the loan in their name, the judge can order the house to be sold.

- Contempt of Court: For willful refusal to obey, a judge can hold your ex-spouse in contempt of court, which may result in fines or even jail time.

- Awarding Attorney's Fees: The court can order the non-compliant party to pay the legal fees you incurred to enforce the original order.

A Motion for Enforcement is not about punishment; it is about achieving the financial separation promised in your divorce. It ensures accountability.

What if the Decree Itself Is the Problem?

Sometimes the issue is not a defiant ex-spouse but a poorly written or unjust court order. If the judge ordered you to assume a mortgage you cannot qualify for, or if the decree is too vague to enforce, an appeal may be necessary. An appeal is not a retrial; instead, a higher court reviews the trial judge's decisions for a major legal mistake, known as a reversible error.

For instance, if financial evidence clearly showed you could not afford the mortgage, but the judge ordered you to assume it anyway, that could be an abuse of discretion. In legal terms, this means the judge’s decision was unreasonable or made without considering the facts and law. An appellate court can correct that mistake.

The specific language in your final divorce decree in Texas is critical. If a flaw in the decree creates an unfair and unsustainable financial burden, you are not trapped by it. Our appellate attorneys specialize in identifying these reversible errors and can build a strong case to help you achieve a fair and practical outcome on appeal.

Common Reversible Errors in Texas Family Courts

You do not have to accept an unfair outcome. In Texas, a judge’s division of property must be “just and right.” If your court order feels fundamentally unfair or is impossible to follow, it may be the result of a significant legal mistake that can be corrected on appeal.

An appeal is not a second trial. It is a focused review by a higher court to determine if the trial judge made a reversible error. This is not a minor disagreement but a mistake so serious that it likely led to an improper judgment.

Plain-English Definition: "Abuse of Discretion"

Appellate courts review property division decisions using a legal standard called abuse of discretion. In plain English, abuse of discretion occurs when a judge makes a ruling that is arbitrary, unreasonable, or made without any reference to guiding rules and principles or the evidence presented. It means the decision was so far outside the bounds of reasonable judgment that it cannot be allowed to stand. Proving this is the core of a property division appeal.

Spotting Common Reversible Errors in the Trial Record

Our appellate attorneys are trained to meticulously review the entire trial record—testimony, exhibits, and rulings—to find these critical errors. Here are examples of reversible errors we often see in cases involving a mortgage.

-

Mischaracterizing Property: A frequent mistake is incorrectly labeling separate property (owned before marriage) as community property, or vice versa. If a judge treated a separate property home as a community asset without supporting evidence, it is a major error that can be appealed.

-

Failing to Properly Value Assets: A just and right division requires accurate valuations. If the judge relied on an outdated appraisal, ignored credible expert testimony, or failed to account for a changing real estate market, the entire property division is flawed.

-

Creating an Unenforceable Order: A divorce decree must be clear and specific. An order for a mortgage assumption that is vague—lacking firm deadlines, a backup plan if the assumption fails, or clear instructions—may be legally unenforceable. An order that cannot be followed is not a just solution.

A judge cannot order a spouse to assume a mortgage they have no realistic chance of qualifying for. If the financial evidence at trial clearly showed they did not meet the lender’s income or credit requirements, forcing the assumption is a classic example of an abuse of discretion that can be challenged on appeal.

Legislative Trends and Lender Hurdles

These challenges are gaining national attention. Recent laws in other states now mandate that conventional loans allow for mortgage assumption during a divorce, provided the spouse qualifies. These laws reflect the reality that many divorcing couples co-own homes. The primary hurdle remains: the spouse must satisfy the lender's strict criteria. You can discover more insights about these legislative changes and their impact.

If the judge in your case ignored clear evidence that you could not meet the lender's qualifications, their order could be a reversible error. An appeal provides an opportunity for a higher court to review that decision and fight for a result that is both fair and financially workable.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation.

Common Questions I Hear About Mortgage Assumptions After a Divorce

Untangling finances after a divorce can be confusing, especially concerning the mortgage. The legal terms and lender requirements can feel overwhelming. Here are straightforward answers to common questions from clients in Texas.

“I Signed a Quitclaim Deed. Am I Off the Hook for the Mortgage?”

No, and this is the single most dangerous misunderstanding in a Texas divorce. A deed—whether a Quitclaim or Special Warranty Deed—only transfers property ownership. It does nothing to affect who owes the money on the mortgage.

The deed addresses ownership, but the mortgage note is a separate contract with the bank. If your name remains on the loan, you are 100% responsible for the debt. If your ex-spouse misses a payment, the bank can pursue you, and your credit will be damaged. The only way to sever this financial tie is through a formal release of liability from the lender, which is achieved through a successful assumption or refinance.

“My Conventional Loan Isn’t Assumable, Right?”

Most people believe this due to the "due-on-sale" clause in conventional mortgages. However, the federal Garn-St. Germain Act creates an exception for divorce. This law prevents a lender from calling the loan due simply because the title was transferred to a spouse or ex-spouse as part of the divorce.

So, yes, your ex-spouse can almost certainly apply to assume the loan. The key is that they must still qualify on their own. The lender will review their finances to ensure they can handle the payments. If they cannot qualify, your divorce decree must include a backup plan, like a deadline to refinance or sell the house. This detailed guide on loan assumption during divorce offers a deeper dive.

“How Long Is This Assumption Process Going to Take?”

Patience is key. The entire process typically takes 60 to 120 days, depending on the lender and your ex-spouse's organization.

The bank treats it like a new loan application, involving paperwork, underwriting, and verification. To keep things moving, the assuming spouse must provide all requested documents promptly. Including firm deadlines in your divorce decree is the best way to ensure your ex-spouse does not delay the process.

“Can I Fight an Order Forcing Me to Assume a Mortgage I Can’t Afford?”

Absolutely. This could be a strong basis for an appeal. In Texas, a judge must divide property in a "just and right" manner. Forcing you to take on a mortgage you cannot afford is the opposite of just. Such a ruling could be considered an abuse of discretion.

An appellate attorney will scrutinize the trial record for evidence that the judge's decision was arbitrary or ignored financial reality. If a reversible error is found, the court of appeals can send the case back to the trial court with instructions to correct the mistake.

This is your protection. You should never be forced to accept a court order that guarantees financial ruin. An appeal is the legal mechanism to correct a fundamentally unfair property division and fight for a resolution you can actually live with.

If you believe the court made a mistake in your family law case, our appellate attorneys can help you seek a fair outcome. Contact The Law Office of Bryan Fagan today for a free consultation at https://familylawcourtappeals.com.